Fed Chair Powell tried to channel Paul Volcker at Jackson Hole. Insiders report that the market’s reaction to his July press conference was to assume that a pivot to easier policy was coming — so he scrapped his prepared remarks for Jackson Hole and instead delivered a short, blunt message that would be harder to misunderstand. “Inflation needs to come down, and we’re going to get the job done even if it causes a recession” was the gist of it.

Further To Go, and Prepare for Some Pain

Has the market gotten the message? Mr Powell put paid to the most recent rally (a bear market rally, as we’d been saying since its inception), and the S&P 500 is back down — not to its June lows, but still 10% off its August highs, and about 17% down for the year. Even so, the “equity risk premium” — the difference between the stock market’s earnings yield and the neutral, or “risk free” rate provided by government bonds — is low compared to comparable historical periods. In simpler terms, that means that the stock market’s overall price-to-earnings ratio probably still has farther to fall.

Of course the other challenge is that earnings estimates have yet to price in the margin pressures that are building across many sectors of the economy as a result of rising input costs (including labor). Managements have often commented recently to the effect that they’ve been able to raise prices to keep pace with input costs thus far — but that they’re reaching the end of that rope. Stock analysts — especially on the “sell side,” where they are employed by companies that want to do investment bank business with the companies they cover — are usually loath to bring down estimates and paint a more dour and realistic picture. Eventually they come around.

These two sides of market valuation suggest that on balance, the market has not yet finished repricing expectations — but it is getting closer. The fact that it’s getting closer suggests some further observations.

Investors Should Pivot — to the Coming Opportunity

It’s been an unpleasant year for investors — especially for those who sought comfort in bonds, or were locked into traditional 60/40 portfolios. Globally, government bonds are on track for the worst year since 1949.

As far as bear markets for stocks go, in the past 140 years, there have been 20 bear market cycles including the present one. On average they see a peak-to-trough decline of 37.3% over a period of 289 days. Although history is only ever suggestive, and not a guide, that average bear market duration would suggest the market has some more downside, but could bottom next month (in October). If it keeps to historical patterns, and the S&P 500 gets perhaps 10% lower, it would be somewhere near where a more normal equity risk premium would put it. While it may not be easy to stomach, all of this simply suggests that what is playing out – despite the intense drama exacerbated by our 24/7 news and social media fixation – is normal.

What’s more, what follows this decline will very likely also be perfectly normal: a recovery from the eventual low, regardless of exactly when that might be. At this point, investors should be focused not on the difficulty of the year thus far, but on the emerging opportunity being created by the reset of prices to more rational levels, the adaptation of businesses and investor psychology to new macroeconomic conditions, and the clearing of excesses and distortions created by extraordinary pandemic-era fiscal and monetary interventions. The bottom line is that the long term data suggest (but does not guarantee nor offer exact timing) that while the average bear market results in a 37% decline, the ensuing bull market recovery produces index returns well over 100%.

Policy Transmission Takes Awhile

Of course, it can take six months for tighter policy to begin working its way through the system — which is to say that the market’s response thus far has been psychological, and we have only just begun to see the “objective” effects. Those objective effects will intensify in coming months. (The Fed only just stopped purchasing mortgage-backed securities, for example.)

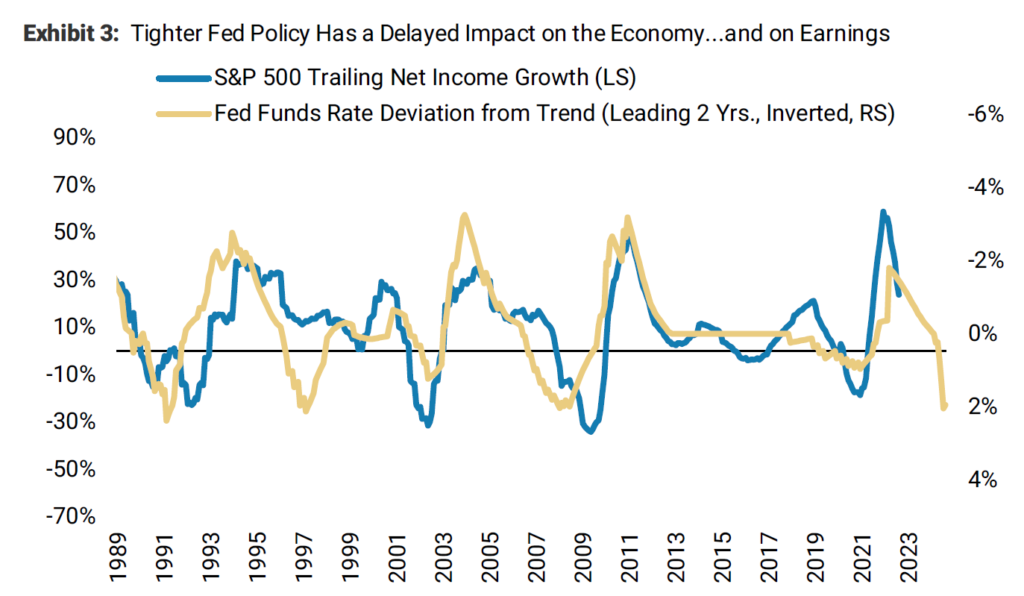

We anticipate that long-duration and speculative assets will continue to be under pressure, and with real rates continuing to rise and the dollar functioning in its traditional role as a safe-haven asset during times of global turmoil, we think gold will remain under pressure as well. The chart below shows that, accounting for a long lag in transmission, sharp Fed tightening episodes correlate quite closely with a deceleration in S&P 500 earnings growth.

Source: Morgan Stanley Research

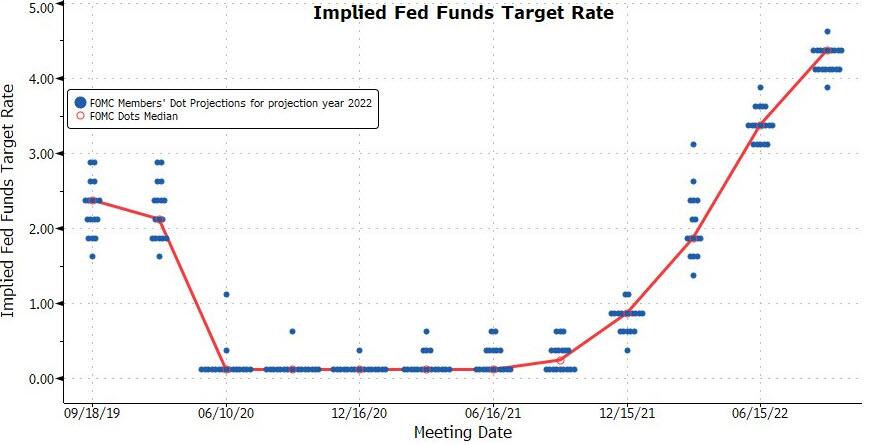

The “dot plot” following yesterday’s Fed announcement of another 75 basis point increase in the Fed funds rate shows it topping out at 4.5% in 2023… according to Fed officials’ consensus, which as we note below, is unlikely to be accurate for the reasons they claim.

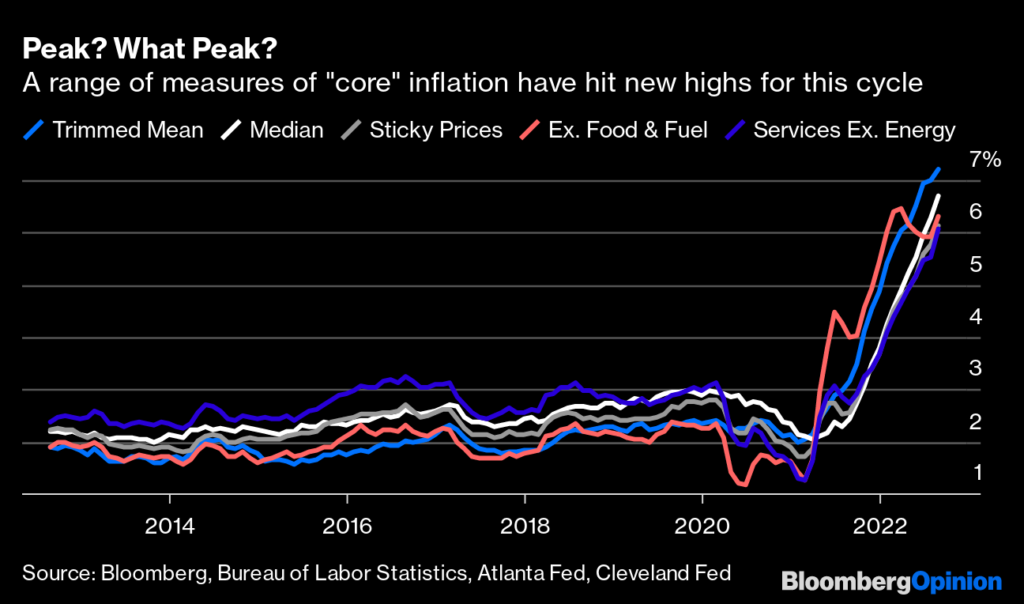

The last round of official inflation data showed how ingrained inflation has become, evident in all the various measures of “core” inflation which desperately strip out volatile elements in an effort to present a more tame picture. No matter how you slice it, it is not tame.

Source: Bloomberg LLP

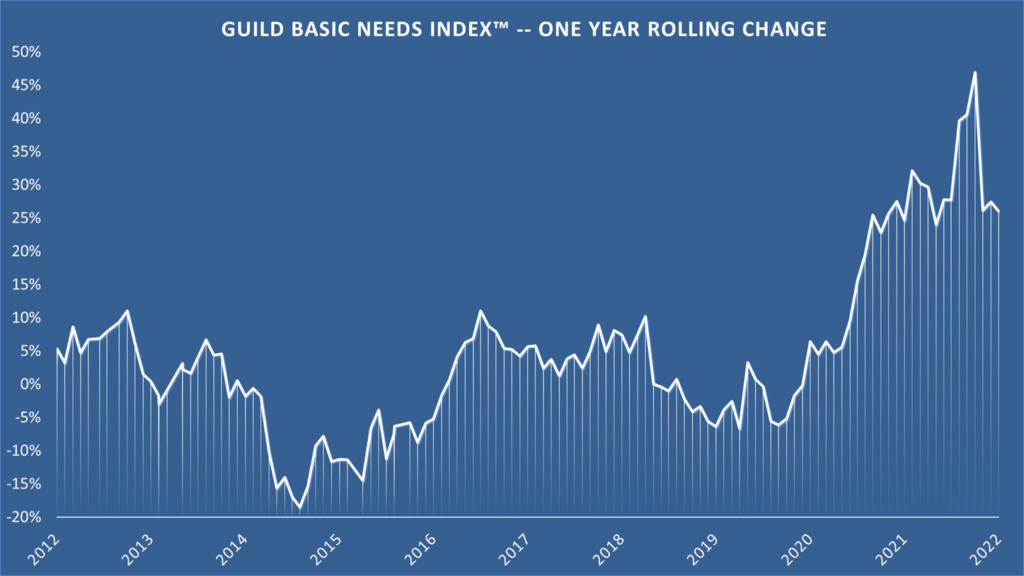

Our in-house, real-world, unadjusted inflation measure, the Guild Basic Needs Index, was at 26% in August — down from its ridiculous highs earlier this summer, but sticking to very lofty, uncomfortable year-over-year levels.

In the coming months, the year-over-year inflation comparisons could moderate as we lap some big early 2022 price spikes; however in our view, it is unlikely that a Fed funds rate at 4.5% would be enough to lay inflation to rest; all other things being equal, the Fed would have to go higher for longer. But all other things are not equal.

When Will the Pivot Happen?

Expectations for earnings are being reset; valuations of assets that depend on long-suppressed interest rates are being reset; slowly, Fed tightening is trickling into the system. All of that is setting up an opportunity for investors; but it is when the Fed pivot really comes into view that the opportunity will be activated.

Therefore, much depends on the timing of the eventual pivot — and there are plenty of events outside the United States that could force Chair Powell’s hand in spite of his determined, hawkish communication. Russia’s partial mobilization of reserves and intention to conduct referenda on the incorporation of occupied Ukrainian territories are one item; the related intensifying energy crisis in Europe (with the full nationalization of German natural gas giant Uniper SE seemingly setting the stage for gas rationing, and the new rise of populist sentiment) is another; unforeseen events in China could be another, whether a negative (aggression against Taiwan, an internal financial or political crisis) or a positive (lifting “covid zero” policies after the October Communist Party Congress). In our view, the biggest risk is a bond market or financial dislocation caused by weak banks in Europe and Asia, and/or by inadequate bond market liquidity in parts of the global financial structure. A big dislocation in either of these areas would cause the Fed to lower rates and increase liquidity in the U.S., and thus the world system.

If the Fed eased off its tightening path as a result of any of these events, it would certainly signal the arrival of a near-term opportunity — even if later, renascent inflation returned for a new round and the whole process got underway again. (That is actually our base case — a relatively short recession now, followed by a pivot and a rally, eventually followed by a renewed impulse of untamed inflation and another recession when the Fed tightens again in response.)

Investors should be planning for the pivot and building their buy list. Leadership will likely be new — although some of the former tech leaders, if they have suffered enough and been kicked to the curb by investors, may be attractive for the rally. In general, we still like scarcity; providers and producers of scarce resources and goods that are made from them; the real and tangible against hopes and dreams; quality earnings, strong balance sheets, and proven dividend growth.

Next week will mark the end of the third quarter. Our plan for next week’s letter is do a video call where we will discuss ideas for portfolio positioning during this volatile environment. We will share what we believe are some important attributes that you want to identify as you build a buy list for the next bull cycle. After all, there is one coming.

Thanks for listening, and stay tuned for more thoughts on where we see places to make money.