We commented in a recent letter that a change in investor sentiment from “catastrophically bad” to “merely bad” could occasion a strong rally. It seems that the end of the third quarter saw sentiment decline to a recent nadir, and the stock market with it. (September is a notoriously difficult month for markets, and this year was no exception — overall, the third quarter alone handed the S&P 500 a 5.3% decline.) Last week, we shared with you a Zoom call that we recorded suggesting that it is times like these — when sentiment is so bad, and investors are frantically positioning themselves so bearishly — that it is time to build a buy list. (Follow this link to view the call and slide presentation.)

Although the primary factors at work all year have been inflation and the rising interest rates being deployed to combat it, there have been plenty of other fears circulating; there have been many “worst case scenarios” that market participants have kept in the backs of their minds, not believing them but not quite dismissing them. Would Europe experience an industrial collapse, or even a collapse in social order, during a cold winter of gas rationing? Would NATO and Russia stumble blindly into World War III with the use of tactical nuclear weapons to defend the newly annexed territories of the Donbas? Would China move against Taiwan after the conclusion of its Communist Party Congress? Would coordinated central bank tightening trigger an unforeseen “Minsky moment” in the global financial system that could cascade through global investment markets — due to some structural flaw to which we are now oblivious, but which financial journalists will be dissecting for decades to come? And of course, perhaps the most significant and realistic of these mostly rather outlandish negative case studies: would central bank tightening simply tip the world into a severe global recession that would tank corporate profits and put the kibosh on any near-term positive outcomes for markets?

That represents a small catalog of some “worst case scenarios” being discussed; and most of them, we must agree are risks — although they are small probabilities, they are nonzero probabilities. The world has conspired to make anxious minds more willing to contemplate them. (The global recession outcome is the most likely of them, indeed a near certainty at this point — though we do not believe it will be as severe as the “worst-case fear” suggests.)

In general, you never want to fight the markets, as it is financially unwise to insist that they are wrong. However, you want to avoid being in the most “crowded trades.”

Spotting crowded trades today can be more difficult since so much activity takes place in the digital world and off the trading floors, but it was clear that at the end of September a few very crowded trades were (1) long put protection against a big decline in U.S. stocks, and (2) bets that the U.S. dollar must keep rising.

As the calendar turned to October, there has been a shift in tone, and some in those crowded trades might have to take some pain.

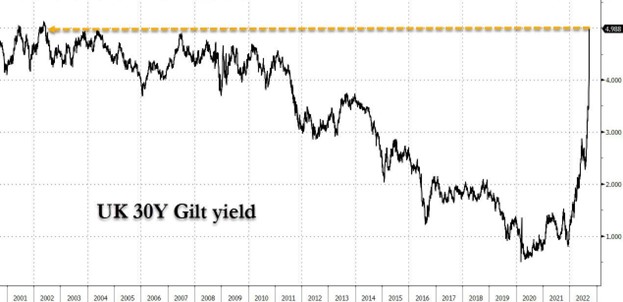

The spark may have been the surprise intervention of the Bank of England to support the UK’s long bond market, and through it, UK pensions. Those pensions were threatened by a catastrophic spike in long-term UK interest rates that followed a “Reaganesque” policy shift from the new government of the UK. The new leader of the Conservative Party, Liz Truss, announced an aggressive package of tax cuts and regulatory reforms to try to ignite economic growth and reclaim the UK’s status as a commercial and financial center. Unfortunately, the market extrapolated these new policies into a highly inflationary future, and long-term UK bonds crashed as a result. The Bank of England, detecting a nascent Minsky moment (in the UK, would that be a “Milton moment” or a “Morris moment”?) of financial instability, quickly intervened by announcing an aggressive program of bond-buying. The fiasco profoundly embarrassed the new UK government.

However, global market participants seemingly took a key and Quixotic lesson from the episode, which was then strengthened by the lower-than-expected 25-basis-point rate increase from the Reserve Bank of Australia. That lesson is: the easing off of coordinated tightening by the world’s central banks is getting closer — if indeed it’s not already just around the corner. The UK is the world’s sixth largest economy — so if tightening has already brought its financial system to the brink of fragility, what does that say about the rest of the world?

This was the obvious justification or explanation for the market’s rally — once again, an anticipation of the ever-elusive Fed pivot, the same phenomenon that sparked this past summer’s market rally that fizzled out in August. We have no more insight into the eventual timing of this pivot than anyone else. But as the market begins to believe that the pivot has grown closer, its willingness to entertain all of the “worst-case scenarios” suddenly evaporates, and we see a bit of animal spirits manifesting underneath the gloom.

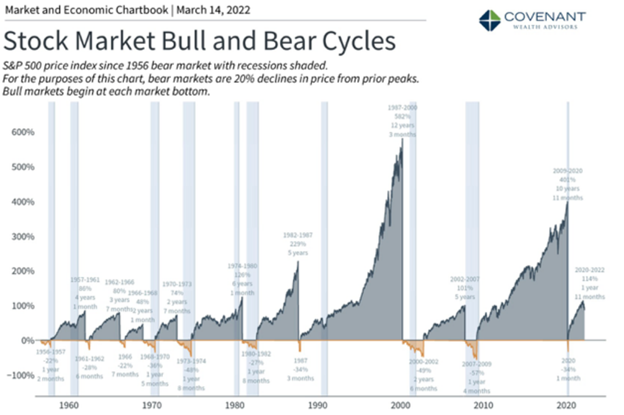

In the above-mentioned recent Zoom call, we made some pointed observations about the perpetual cycle between market bull and bear phases. We are now enduring a bear phase, and the truth is that the bull phases that follow a bear decline eventually dwarf those declines for the investors who maintain their composure and their willingness to be, as Warren Buffet likes to say, “greedy when others are fearful.” The chart below does not extend past the first quarter of 2022, and so does not include the most recent part of this year’s bear market; but it is illustrative of the reason why stocks, in spite of their volatility, remain the most robust wealth-creation tool the world has ever seen.

Source: Covenant Wealth Advisors

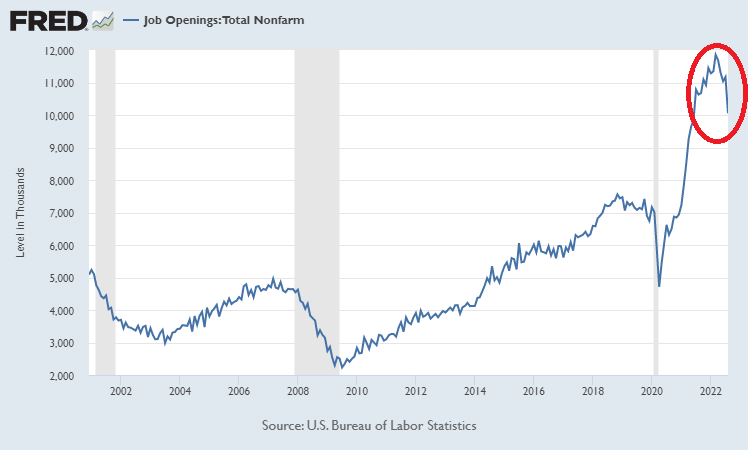

When the fear of worst-case scenarios is off the table, markets are more free to rally from levels created by excessive fear. However, when worst-case scenarios come off the table, and some sobriety in risk analysis settles in, more realistic risks can come into focus. We still believe that a moderate recession is such a risk, and that as it comes closer, analysts will begin to dial back future earnings estimates that still remain too high for many businesses. Tomorrow will see a very consequential indicator of whether the Fed’s tightening is resulting in negative economic consequences: the September BLS employment data. It is worth noting that preliminary job openings JOLTS data published earlier this week indeed showed that the white-hot labor market is weakening, with job openings a million below the number that was expected.

Source: Federal Reserve Bank of St Louis

On balance, in spite of Fed Chair Powell’s bucket of cold water at Jackson Hole, we do believe that the Fed, which is now inescapably political, is still attentive to meat-and-potatoes issues — particularly the labor market. Of course, a true European “Minsky moment” would certainly call forth a Fed response if it occurred. Which might come first remains to be seen. A deteriorating labor market alone would call forth political pressure, but might not be enough to get the Fed to balk at further tightening.

In any event, we believe that the eventual Fed pivot will occur before inflation has been vanquished. Given the higher leverage of the U.S. and global economies in 2022 compared to 1980, its capacity to bear high and rapidly rising interest rates is considerably less. In the 1970s, further, it took several rounds of tightening and failure before the Johnson administration’s “guns and butter” driven inflation was finally dispelled — and several rounds of market decline and rally. That may well be the pattern that emerges in coming years.

Our takeaway? Don’t get sucked into either despair or euphoria. The despair starts with realistic concerns, and expands to encompass unrealistic fears of highly unlikely events. The euphoria tends to obscure realistic and sober analysis of the emerging objective consequences of the most powerful policy-makers — which under current circumstances are the fiscal and monetary authorities of the United States. There are realistic concerns to work through — and a bull phase on the other side of them, likely one that will include leadership in areas neglected during the last bull run.

Thanks for listening; we welcome your calls and questions.