Looking for outperformance in Asia’s emerging economies can be a risky undertaking. The trade conflict between the United States and China is generating one set of uncertainties. More deeply, there is the problem of China’s fraught transition from an industrial-led to a consumer-led economy, and all the domestic political stresses that is creating. Supply chains are being reconsidered; resource exporters who have relied on an insatiable Chinese appetite for raw materials are being challenged. In a way this is par for the course for Asian emerging markets, and indeed, for emerging markets in general, where the prospect of robust economic and corporate profit growth goes hand-in-hand with structural growth pains, political and financial turmoil, and political risks of various kinds. These are not markets for the faint of heart.

However, there is another, subtler opportunity we see in Asia, and it is one that has not yet attracted a great deal of attention from the world’s investors. We refer to one of the developed Asian markets: Japan.

Great enthusiasm greeted the election of Prime Minister Shinzō Abe in December, 2012. He inaugurated a new economic and financial regime — dubbed “Abenomics” — in an attempt to jolt Japan out of a long period of deflation.

Abenomics — Fireworks, But Slow To Bear Fruit For Investors

Abenomics was a three-pronged approach: monetary easing, fiscal stimulus, and structural reform. The first two prongs have been accomplished with fireworks, with the Bank of Japan still engaged in the world’s biggest QE program. Abe just announced a $120 billion fiscal stimulus plan, the biggest since the global stock market turmoil and economic slowdown in 2016. This plan would help combat the effects of a recent sales tax hike, and should boost Japan’s GDP by a cumulative 1.4% through 2022.

The structural reform effort has been less prominent, and Abenomics has not given foreign investors stellar results overall. Japan’s stock market, in U.S. dollar terms, has lagged behind the S&P 500 since Abe’s election.

Global investor interest in Japanese equities still lags, in spite of the Japanese market’s relatively inexpensive price-to-earnings ratio. As we write, the MSCI Japan index, tracked by the iShares MSCI Japan ETF [NYSE: EWJ] trades at a P/E ratio of 14.3 times trailing 12-month earnings, compared to 22.3 times for the S&P 500 — a 36% premium.

Japan, of course, is one of the world’s leading economies. Many Japanese firms are global leaders; the country has a first-class legal and political framework, including the rule of law, an independent judiciary, and robust protection for property rights. Like the Germans, the Japanese labor force has a reputation for hard work, discipline, and devotion to precision and excellence in high value-added manufacturing.

So what accounts for the unwillingness of global investors to bid for Japanese stocks? And could that valuation gap close?

Challenging Demographics

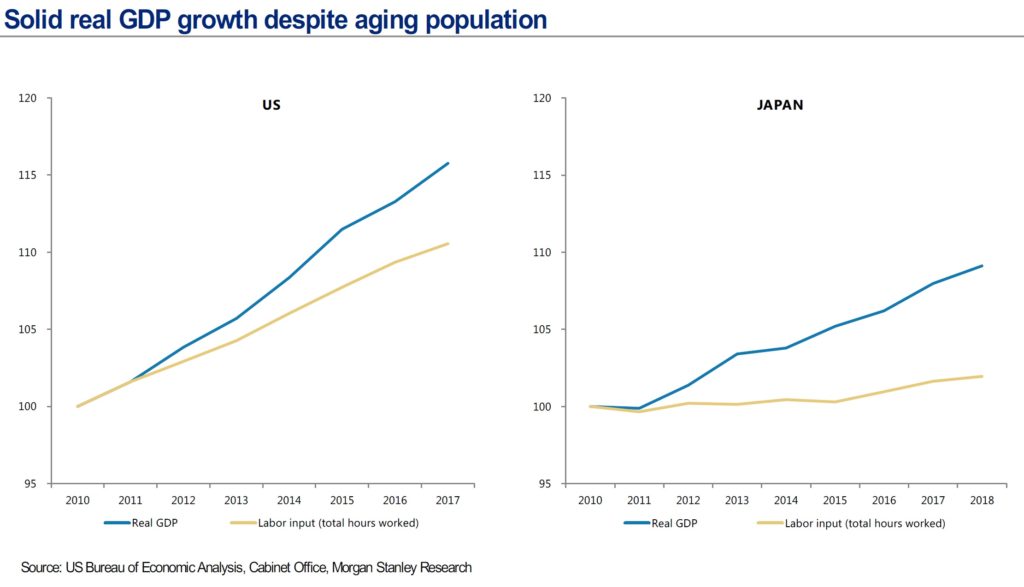

Analysts often cite Japanese demographics as a particular challenge faced by Japan’s corporates. The country’s aging and shrinking population is thought to be a headwind to growth, and unlike other countries facing similar problems, Japan has some political and cultural resistance both to immigration and to the expansion of women’s role in the labor force.

That in itself, though, doesn’t need to derail economic or corporate profit growth. In fact, given the slower growth in labor hours worked than that experienced in the United States, Japan enjoys a relatively larger “bang for the buck” in terms of consequent GDP growth.

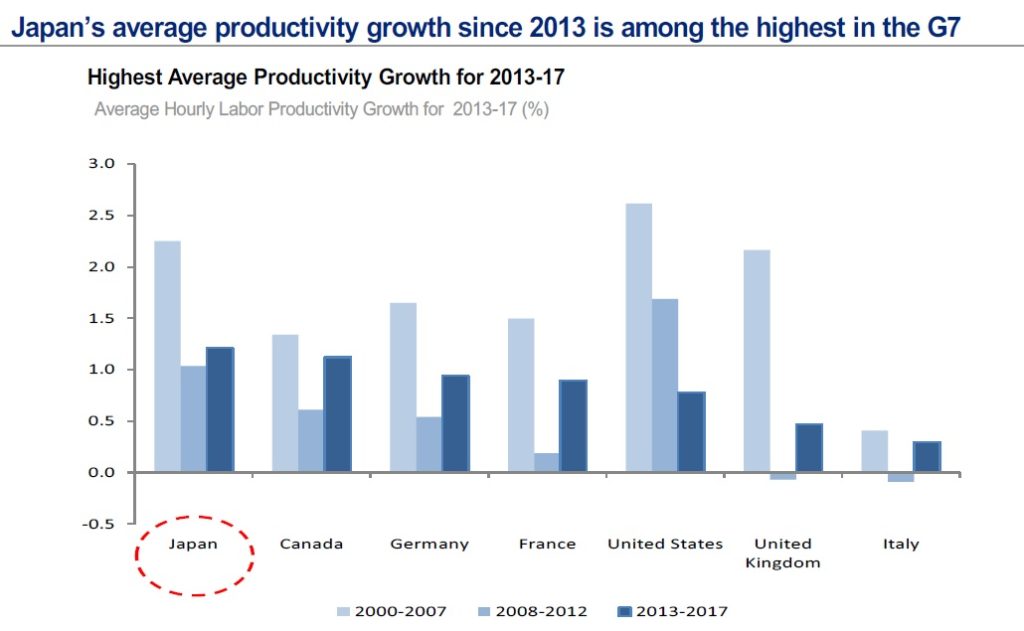

Part of this is due to greater productivity gains thanks to Japan’s leadership in robotics and automation.

Corporate Governance

Still, it is not only these demographic concerns that weigh on global investors’ minds when considering Japanese equities. A significant part of the valuation gap derives from the perception that corporate governance standards in Japan leave much to be desired compared to those of Europe and particularly the United States. These matter to investors, who need to feel that corporates take them seriously as stakeholders if they’re going to give companies a decent valuation.

Indeed, it’s not just a perception… There are many problematic aspects of corporate governance in Japan. And while QE and other fireworks have garnered the most attention in Prime Minister Abe’s reform efforts, it is likely the slow, long-term structural reforms to Japanese corporate culture and governance that may begin to close some of the valuation gap with American firms — and may allow Japanese corporates to boost performance metrics such as their return on equity, by encouraging a better deployment of corporate cash.

What are some of the main areas that needed to be addressed, and how has the Abe administration been moving Japan’s corporate governance in the right direction during his tenure as Prime Minister?

- First, the composition of corporate boards has been inadequate, lacking sufficient long-serving independent board members.

- Second, companies have tended to cluster their annual general meetings on two or three days during the year, making it impossible for investors to participate effectively. Company communications were rarely in English.

- Third, the country lacked until recently a unified national code for corporate governance. The lack of standards often spelled trouble for minority and foreign shareholders, and hindered them from exercising their rights.

- Fourth, many Japanese firms have excessively high family ownership and cross-ownership with other companies — the kind of opaque structures that often work against minority shareholder interests, and against better financial performance.

Since 2013, the Abe administration has attacked these problems from several angles, and slow progress is being made.

Leveraging the Influence of Japan’s Government Pension Fund

Japan’s Government Pension and Investment Fund [GPIF] is one of the world’s largest, with nearly $15 trillion in assets under management. The GPIF was one of the first signatories of a new Stewardship Code encouraging institutional investors to press the companies in which they invest to have better governance practices. The participation of the GPIF was a key milestone and put pressure on Japanese institutional investors to join. The GPIF itself is incorporating global governance standards into its investment process.

A New Index For Good Corporate Citizens

In 2014, the Tokyo Stock Exchange launched a new index, the JPX Nikkei 400, which consists only of companies that conform to a list of global investment standards, including companies’ efficient use of capital. (That index is tracked by a relatively illiquid fund, the iShares JPX Nikkei 400 ETF [NYSE: JPXN].)

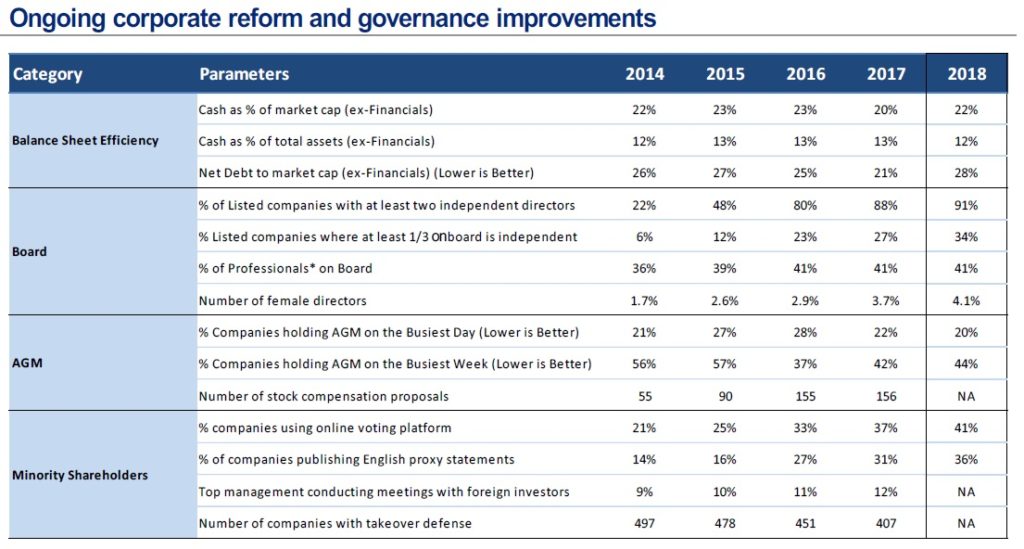

In 2015, Japan Exchange Group [JPX], which owns the Tokyo Stock Exchange, released a voluntary corporate governance code more in line with global standards, that applies to all companies listed on the exchange. The pressure for compliance has led to gradual improvement in the code’s metrics. In 2015, 11.6% of listed Japanese companies were compliant; by 2017, that had risen to 25.9%.

Other new rules have strengthened disclosure requirements and reduced the opportunity for the distribution of material insider information.

Cross-ownership of Japanese companies remains an area of difficulty, where relatively little improvement has been seen, and progress remains to be made in boards’ gender diversity and in foreign-language communications by management.

Gradual Improvement

In general, though, these efforts have begun to bear fruit — although we note that such cultural shifts are long-term phenomena and we would not expect sudden and drastic change. But still, positive changes are afoot:

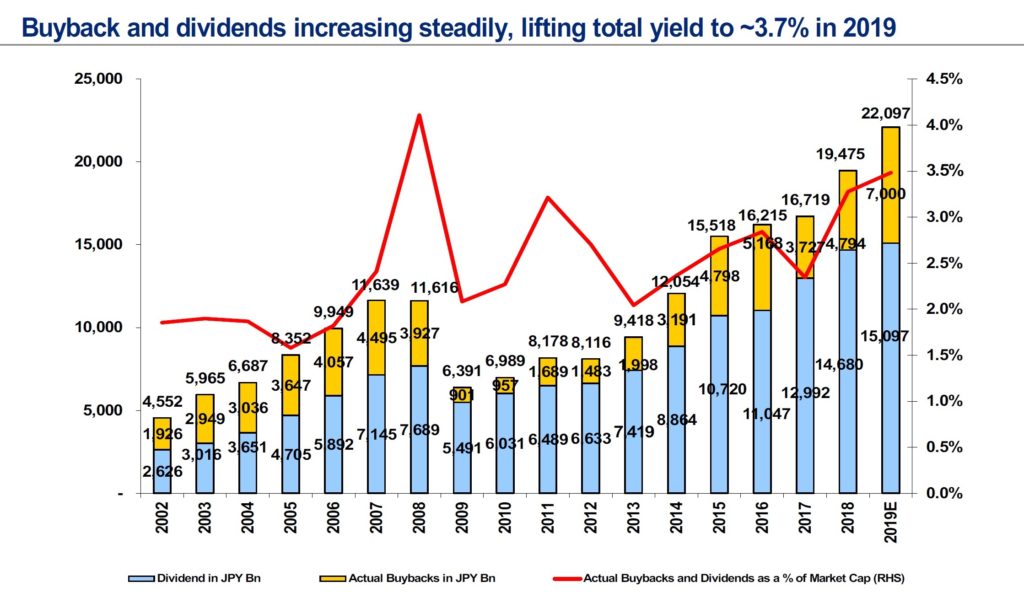

And where the rubber meets the road, shareholder-friendly cash deployment such as buybacks and dividend payouts have begun to rise:

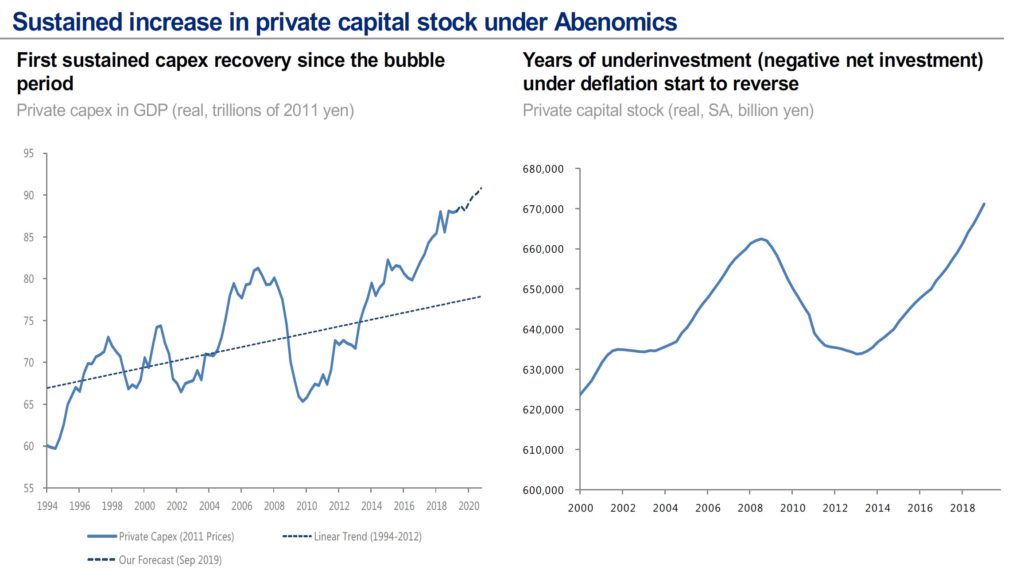

So has capex, showing that better governance is leading to a more productive use of cash:

Investment implications: A big new fiscal stimulus should help boost Japan’s economy in the coming year, and overcome some negatives of the recent sales tax hike. Longer term, positive changes are afoot in the governance of Japan’s corporations — changes that have the potential to gradually close the valuation gap between segments of the Japanese and U.S. stock markets. These changes may ultimately be one of the most significant of Prime Minister Abe’s legacy, at least from the perspective of foreign investors. In spite of perceived demographic challenges, a valuation catch-up by Japanese corporates could be a long-term theme favorable to Japanese stock exposure.