We recently read a piece in Bloomberg on a notable long-term trend: the U.K. stock market is shrinking. Looking back to 2016, John Authers notes:

“While the index has risen more than 23%, the total value of shares has increased by only 2.7%. The reason is the ebbing importance of stock markets as a way to raise money. Companies aren’t bothering to issue new shares, but instead going to private equity companies; buying back their own stock; or selling out altogether to nonpublic investors. All these measures affect the size of the market, but don’t hurt the value of individual shares within it, which is what drives indexes. Indeed, many of these measures help drive up share prices. But if large institutions want to gain access to the full range of opportunities in the British economy, they need to take stakes in private equity. For individual investors, for whom investing in private equity remains virtually impossible, their opportunity set shrinks…

“The London Stock Exchange offers us the world of contemporary shareholder capitalism in a nutshell. The money goes to indexing groups and private equity operators while the sum of equity capital shrinks. But normal investors, thanks to the financial engineering that pushes up share prices and the low costs of index investing, are doing OK for now. Let’s hope it stays that way.”

Authers sums up an observation that has been made often over the past few years, not just concerning the U.K. stock market, but concerning most developed-world markets, including the United States.

The argument is that public stock markets have experienced a deep, long-term decline in the number of listed companies, mostly due to (1) easier regulations surrounding the raising of private capital, (2) more onerous compliance regulations for publicly listed companies, and (3) the unproductive “short termism” that sets in when management has to worry about missing Wall Street earnings targets every quarter.

Those, like Authers, who see this trend as a problem, observe that it helps drive indexing, reduces opportunities for normal investors, may be leading to risky market concentration, and overall, hands a bigger share of the wealth created by free-market capitalism to a smaller set of actors — primarily index managers and private equity firms and their well-heeled investors.

In the long run, critics fear, it could create unforeseen systemic problems — for example, by reducing the rewards of bottom-up research, it reduces the amount of such research that is being done, leading to markets that ultimately are flying more and more blind about their component companies’ real underlying value. If shrinking markets and indexing mean that less real value discovery is being revealed in market prices, that could ultimately contribute to more severe market dislocations (read “crashes”).

There is certainly some truth to this analysis, and to these concerns. But the reality may not be as dire as the critics fear.

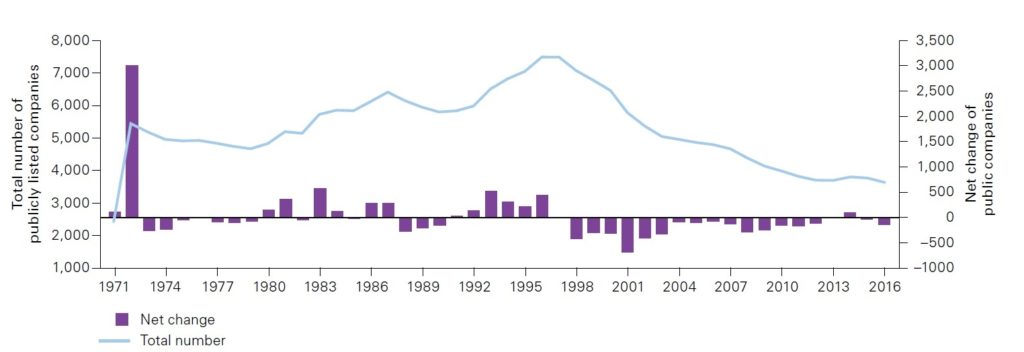

For one thing, identifying a decline as a “decline” depends on the timeframe. Many analysts who look at the declining number of companies are using a baseline that seems to be historically elevated. Looking at the number of listed companies in the United States in a longer time-frame shows a slightly different picture:

The big spike in listed companies in 1972 corresponds to the creation of the NASDAQ exchange, an event which lead many formerly OTC-traded stocks to join the ranks of publicly traded companies.

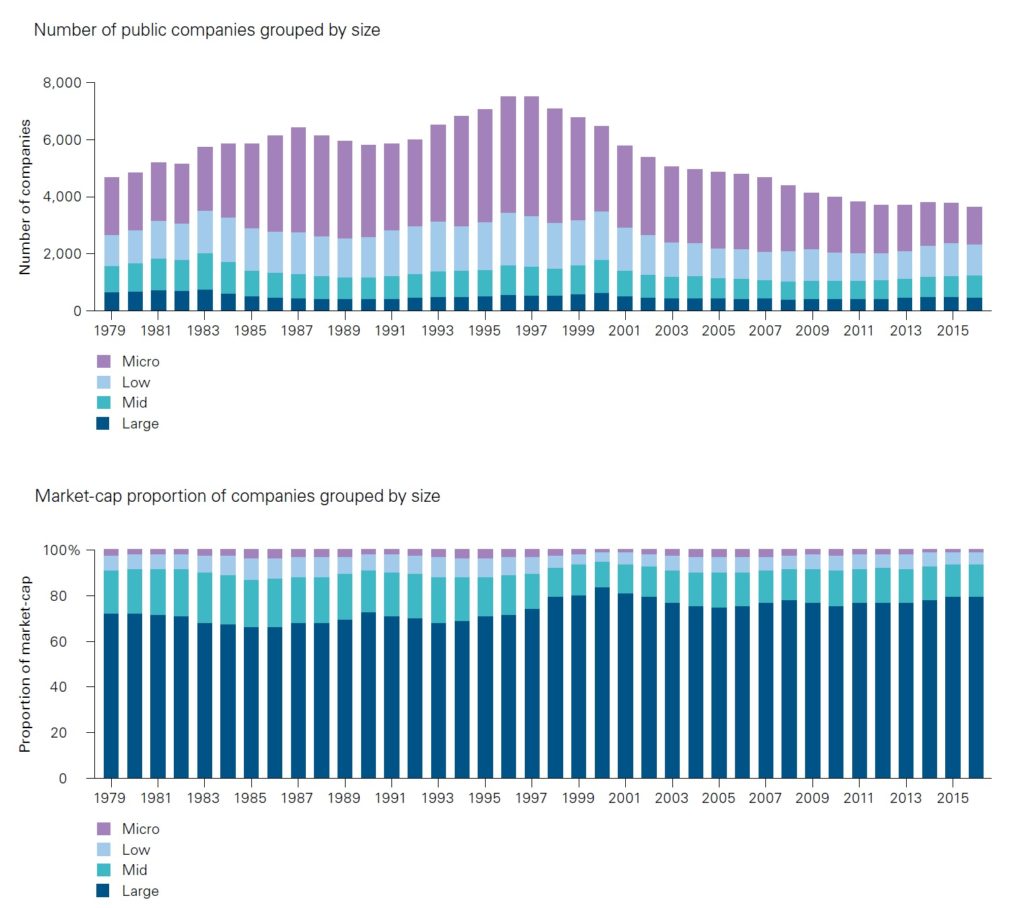

Another observation is that the distribution of the “missing companies” matters a lot as well. In other words, from what part of the “capitalization stack” are companies delisting, or choosing not to publicly list? It turns out that the phenomenon mostly affects microcaps.

Strip out the microcaps, and the situation looks less alarming. It is important to remember that while a few microcaps are highly successful and go on to rise in the ranks, becoming small, mid-sized, and larger companies, the vast majority fail and are delisted, or are acquired by larger competitors.

In short, in historical perspective, its the 90s heyday of microcaps that decisively ended with the Dot Com crash that looks like the anomaly, rather than the current relative dearth of such companies as options for retail investors.

Indeed, from the perspective of normal retail investors, the current trend has some benefits. While publicly traded microcaps offer opportunities for outsized gains, they also offer opportunities for outsized losses (witness the patchy track record of venture capital itself, where really only the top quartile of funds outperforms the broad market), and retail investors without research expertise and a healthy dose of good fortune have always had a hard time there.

The increasing tendency of small companies to seek funding from venture capital, rather than the private market, and to “exit” by M&A rather than a public listing, means that they enter that public market as parts of established, older, slower-growing companies. Ultimately this will likely mean that markets exhibit lower volatility, other things being equal — a bane for nimble traders (witness the challenged performance of many investment-bank trading desks of late), but a boon for more plain-vanilla retail investors.

Investment implications: The trend for a smaller number of publicly listed companies in many developed markets poses a challenge for investors and speculators who seek to capitalize on the growth potential of very small, disruptive start-ups — and tends to send the gains (and losses) from such investment to private equity and venture capitalists. Retail investors have less to fear from this trend — though in the very long run, the attrition of careful, independent analysis, and the continued rise of indexing, may contribute to future problems.