As we noted last week, some of the social and economic changes wrought by the covid pandemic will be enduring and not just transitory. Many companies well-positioned to benefit from these new or newly strengthened themes have seen their stocks outperform in the year so far, and although volatility certainly lies ahead, we believe that this trend will likely continue. Last week we discussed companies in the e-commerce and financial technology industries. This week, we’ll give a few words to healthcare — both the emerging industry delivering medical services online (telemedicine), and the overall regulatory landscape.

Politics and Healthcare

Healthcare has been a political flashpoint for decades, and the current hyper-partisan political environment has raised mere conflict to the level of endemic hostility and antagonism. Potential outcomes such as Medicare for All are on the table, which would have existential consequences for most industries in the healthcare sector. Although the more radical options are still politically far-fetched, they are obviously becoming less so. We believe the large political and social arc is towards greater government intervention in healthcare. This will gradually, over a period of years or decades, with advances and declines, make healthcare a less rewarding investment. Any investor knows this who considers the contrast between highly regulated European pharmaceutical companies and the much more dynamic and innovative U.S. biopharmaceutical industry.

Of course, there are exceptions, and we are making no judgements about the social desirability of this trend. We are simply noting that for investors in the U.S. healthcare sector, monitoring this political process is of primary importance. The policy “weather” surrounding U.S. healthcare is now, and will become even more, the basic structure which determines how much investors are willing to pay for the stocks of healthcare companies — and therefore the basic structure that shapes your investment success in this sector.

We believe that the covid pandemic is creating a significant change in the political environment, and has changed, at least temporarily, the trajectory of the healthcare debate.

Covid and Drug Pricing

One central aspect of healthcare’s political fracas has been drug pricing. Here, biopharmaceutical firms have been punching bags in the media — certainly at times understandably so — and drug price legislation has been a theme on both sides of the aisle. Most of the world outside the U.S. lives under drug price controls of one form or another. These rules generally result in lower costs for prescription medication for consumers.

However, they also result in more constrained biopharma R&D budgets. Thanks to the pandemic, biopharma R&D is moving from the “bad guy” category of the public imagination to the “good guy” category — and if it’s moving in the public imagination, it’s also moving in the minds of the people courting their votes. All of a sudden, the electorate is realizing that their deliverance from a clear and present danger may depend in part on women and men in white lab coats working in laboratories funded by drug companies. The “powerhouse of pharma innovation” is no longer a slogan which voters cynically assume conceals marginally useful products, patent gaming, and price gouging — it has once again become a sentiment of genuine praise and gratitude for many.

It’s hard even to remember now that at the beginning of the year, significant drug price legislative activity had been expected in the first half of 2020. Various legislative proposals are still on the table, but the timeline has shifted to post-election, and the topic is unlikely to figure significantly in the campaign.

We believe also that the pandemic experience will reshape the debate, not just about drug pricing, but about healthcare economics in general. We believe that the need for balancing consumer healthcare costs with the ability of the healthcare sector to fund ongoing research and development is already becoming more broadly appreciated by the public and by politicians.

As the pandemic continues, we believe that it is likely to continue to moderate, with hospitalizations and mortality continuing a gradual stop-and-start decline. There will be more infections, but these are already skewing towards the lower end of the age demographic where the infection fatality ratio is actually quite low. This is what we would expect as we navigate the passage to “herd immunity” and try to balance normalcy of life for the majority who are at low risk, with protection of the most vulnerable.

Still, in the absence of a vaccine and decisively effective treatments, pandemic concerns will remain an uneasy mental backdrop for many people who are worried either about themselves or about loved ones. We think that this attitude is likely to last beyond the election, and dampen popular enthusiasm for any healthcare reform that paints healthcare corporates as enemies.

Telemedicine

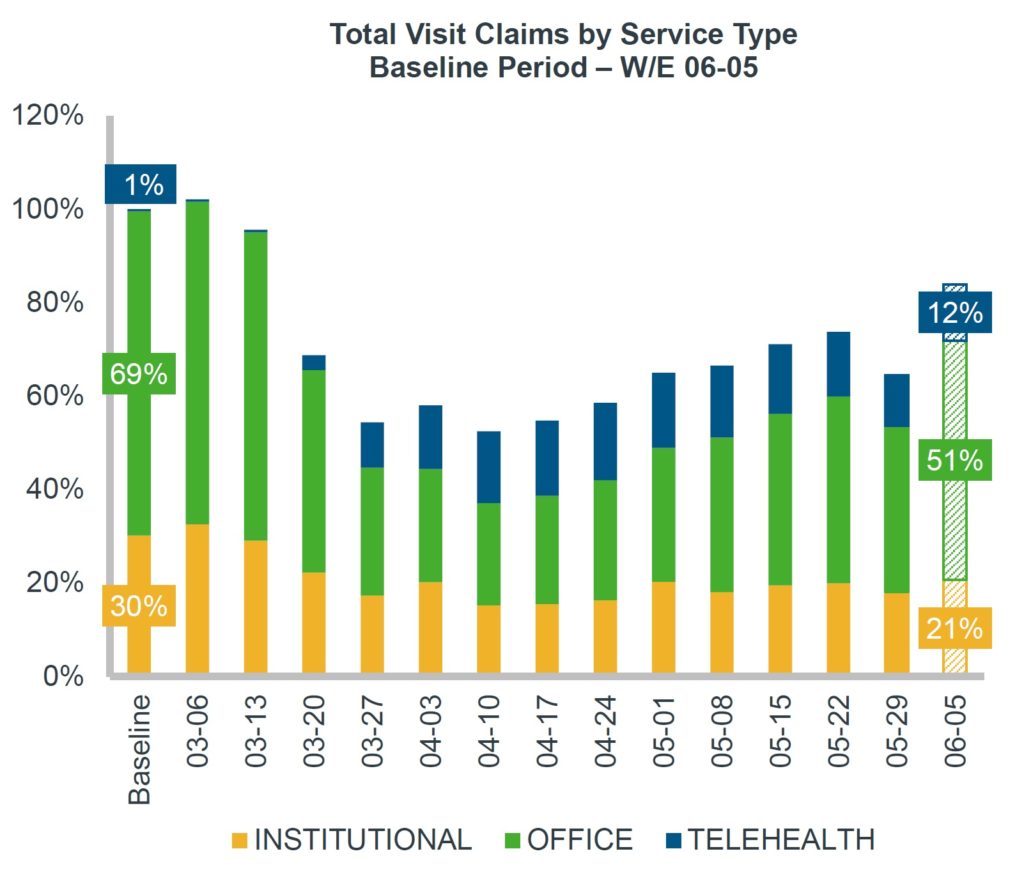

Biopharma is not the only industry within the healthcare sector that’s been directly important to the pandemic response. Another area that has garnered significant investor attention is telemedicine — the online delivery of healthcare services. Predictably, the onset of the pandemic caused virtual healthcare interactions to skyrocket — from a baseline of about 1% of visits, to about 12%.

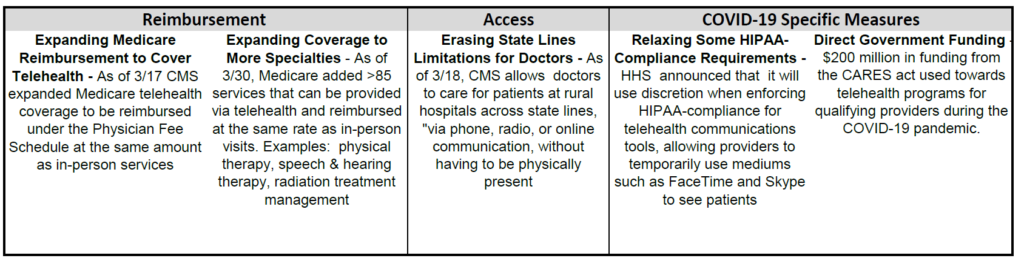

Why could this change be lasting? First, because physicians and patients using telemedicine for the first time are reporting broad satisfaction with the experience. Second, because this medium for healthcare delivery drives lower medical costs, benefitting healthcare payers such as insurance companies. Third, because the Centers for Medicare and Medicaid Services (CMS) acted rapidly and aggressively at the beginning of the pandemic to reduce regulatory barriers and make it easier for healthcare providers to bill for these services.

While the pandemic may give biopharma a stay of execution, it will probably give telemedicine a major promotion. The various positives for physicians, patients, and payers may mean that telemedicine accelerates its move towards becoming a “standard of care” across the healthcare spectrum.

As a consequence, other digital healthcare technologies are also likely to see a lasting upward inflection in their adoption trajectories. Many chronic conditions can be monitored digitally — particularly diabetes. The adoption of digital monitoring solutions for diabetics makes direct sense in the context of the pandemic, since diabetes is one of the primary co-morbidities that puts people at risk for serious covid complications. It also makes sense as part of a secular adoption of telemedicine, since physicians will be able to seamlessly integrate remote monitoring into their remote provision of care. While there are pure-play options in this area, investors should not neglect the two tech mega-caps who have the demonstrated interest and the product infrastructure to be key players: Apple [NASDAQ: AAPL] and Alphabet [NASDAQ: GOOG].

Investment implications: Telemedicine’s adoption curve has inflected upwards, and the theme will likely prove to be an enduring beneficiary of the changes wrought by covid. While companies such as Teladoc [NASDAQ: TDOC] are obvious participants in the theme, companies such as CVS [NYSE: CVS]; insurers such as Anthem [NYSE: ANTM] and Humana [NYSE: HUM]; tech giants such as AAPL, GOOG, and Microsoft [NASDAQ: MSFT]; and digital health tech firms such as Dexcom [NASDAQ: DXCM] will all have significant roles to play.

Please note that principals of Guild Investment Management, Inc. (“Guild”) and/or Guild’s clients may at any time own any of the stocks mentioned in this article, and may sell them at any time. In addition, for investment advisory clients of Guild, please check with Guild prior to taking positions in any of the companies mentioned in this article, since Guild may not believe that particular stock is right for the client, either because Guild has already taken a position in that stock for the client or for other reasons.