For some time the market’s action has reminded us of a verse from the New Testament:

For whoever has, to him more shall be given, and he will have an abundance; but whoever does not have, even what he has shall be taken away from him.

Matthew 13:12

(Of course this verse expresses a truth about the world that long predates covid, however much people might not like to hear it.)

This certainly seems to be the case for much of the stock market right now. There is a widespread narrative that the stock market has come unmoored from underlying economic realities, and is floating in blissful abandon on an ocean of central bank liquidity. But if the quotation above is the case for large parts of the real economy as well, that might mean that the stock market is in fact being quite rational. It’s recognizing an emerging reality… which is, after all, part of its job. Investors who want to avoid shipwreck would be advised to pay attention to what the market is telling them.

Living With Covid

We believe that for many, if not most, Americans, the worst of the pandemic fear is behind them. As a country, we are acclimating to the new reality — whatever we believe it to be. To us the data suggest (1) that the pandemic is moderating, and (2) that the depths of fear surrounding it were driven by a lack of clear understanding of its severity, mortality, and likely outcomes.

The pandemic’s moderation is suggested by gradually declining mortalities and dramatically declining hospitalizations on a national level, trends which are maintaining even as states and localities remain open and continue to move towards further re-opening.

The initial fear is receding thanks to an understanding of the great disparity in risk faced by different demographic groups, as well as more effective treatment options.

There are many risks that people take in daily life with little reflection — from getting in a car for their daily commute, to insulting a stranger. Covid is on its way to becoming just another one of them.

What Shape Recovery?

Late March and early April saw dramatic financial-market interventions which reassured investors. Equally dramatic action from the U.S. government supplemented unemployment benefits and offered support to shuttered businesses to retain staff. With immediate catastrophe seeming to be off the table, the debate shifted to the shape the recovery would take. The optimists suggested a V — believing that the economy would snap back thanks to monetary and fiscal intervention, and “warp-speed” vaccine and therapeutic development. Less sanguine observers suggested a U- or W-shaped recovery; the truly pessimistic opted for an L.

Lately, though, many observers have been calling for a K. A K-shaped recovery would be bifurcated — a sharp decline, followed by a sharp uptrend for some, and a sharp downtrend for others.

For the stock market, that is not far off the mark. The chart below shows the divergence between the FAAMGs (Facebook, Apple, Amazon, Microsoft, and Alphabet) and the lowly small-caps of the Russell 2000 index. Not quite a K — for that you would need to compare the FAAMG stocks to oil stocks — but you get the idea.

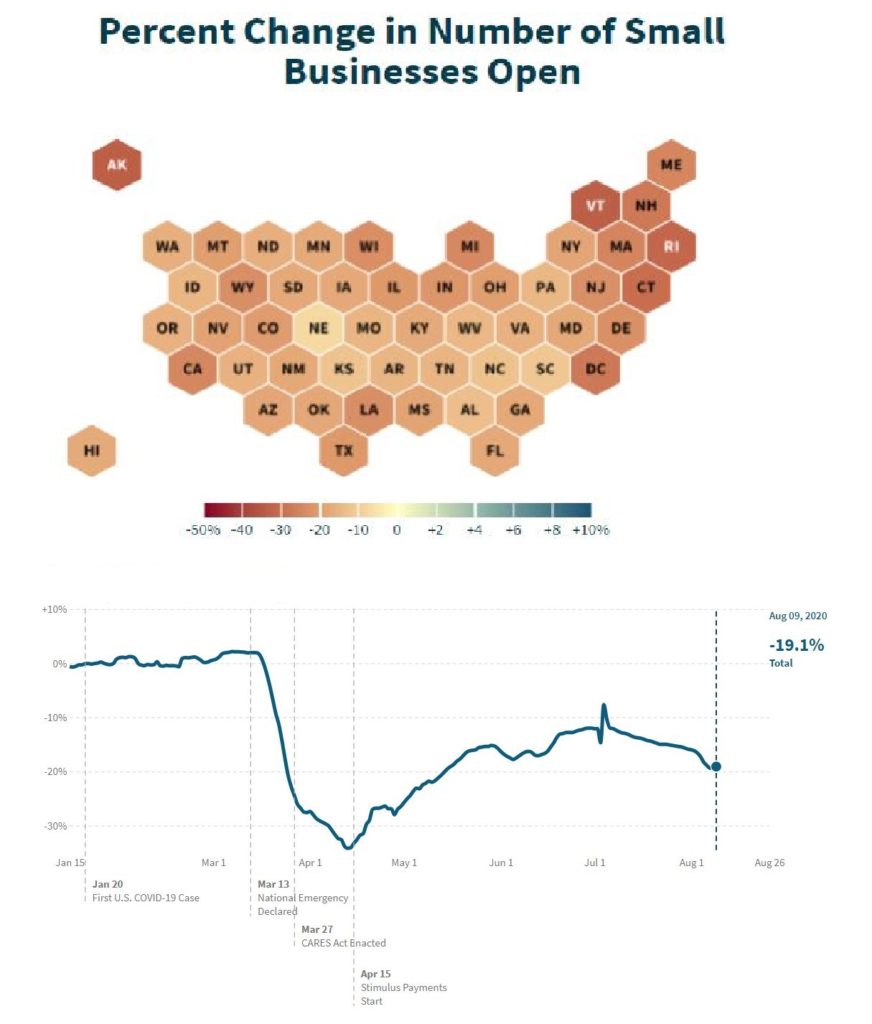

If the FAAMGs show us the victory of the large, the state of small businesses may show us the fate of the others; as of early August, according to analysts at Harvard and Brown Universities, 19.1% of U.S. small businesses were closed — reporting no financial activity — and trending down.

This bifurcation is replicating across the U.S. economy, across economic sectors, across geographies, and across job descriptions and socioeconomic groups. Companies, sectors, industries, states, municipalities, and jobs affected positively by the pandemic-engendered shifts are booming — and others are lagging.

What seems to be happening is that the policy response to the pandemic has served to intensely accelerate trends that pre-existed it, compressing years’ worth of change into a period of a few months. The beneficiaries of those trends are booming, and if they are publicly traded companies, their stock prices reflect it.

It is not just stock-market investors who should pay attention, because these accelerated shifts will affect a wide range of assets.

The Accelerated Changes

We can group the key shifts into four areas. In each case, they have been intensified not so much by the pandemic as by the policy response to the pandemic. Further, since they have accelerated pre-existing trends, rather than creating new ones, those trends are unlikely to revert even if the pandemic continues its gradual moderation — indeed, they are unlikely to revert even with the advent of a vaccine. They may become less intense, but they will likely continue. The market’s big winners have all been on the winning end of these accelerated changes.

First: telepresencing. In essence, remote work and collaboration is a form of automation. It is using technology to avoid expensive, risky, or inconvenient human activity: in this case, travel, and time spent in expensive-to-maintain real estate in cities. It is not as dramatic as factory automation but it is in the same family.

The limitations of telepresencing are being discovered — close-knit teams are feeling the stress from a lack of in-person collaboration. But many, many companies are discovering that remote work is as productive as office time, and a lot less expensive. (Workers may not agree, especially as they suffer the psychological effects of social isolation, but they’re not paying rent in an office tower.) This will have profound effects on the economics of much commercial real estate, and will be disruptive to real estate in dense urban centers more broadly. Even if we “get back to normal” on the virus front, or something resembling it, businesses will not unlearn what they just learned about how much of their workforce they don’t need to house in an expensive office. U.S. employers project that even after the “end of covid,” days worked remotely will triple.

This will also mean job polarization. Knowledge workers, and others who just realized that their jobs can be seamlessly ported to a room in their home, will be head and shoulders above their peers in the service occupations. And those unemployed whose trade can “telepresence” are already much more likely to find new work.

Second: urban changes. The flight of workers from dense urban areas will change the economics, and potentially the politics, of those areas profoundly. We are not suggesting anything as dramatic as the “death spiral” that some have suggested for cities like New York — with office-worker flight killing service businesses, reducing tax revenues, challenging municipal finances and services, and driving more business out of town ad nauseam. But those who own commercial real estate in dense urban areas should consider that an enduring change of trend may be unfolding. If your investment portfolio is concentrated in commercial real estate, you should contemplate how you could diversify.

Third: employment dominance by large firms. Large businesses are simply more resilient to mandatory shut-downs than their smaller peers; the data cited above show that small companies are already experiencing disproportionate closures. From a large-scale perspective, since big firms tend to pay out less of their earnings to workers, this could shift the national structure of income distribution. This, combined with what could be persistent unemployment in the lower quintiles of the wage scale, could exacerbate politically volatile sentiments surrounding inequality, since even when retirement accounts are considered, only half of Americans own equities. Hedge fund investor Ray Dalio already pointed out last year that the political consequences of perceived inequality could be very dangerous. This is another risk that investors should keep in mind. It could be one of the major tertiary effects of the pandemic.

Fourth: accelerated automation. In a lot of service industries where telepresenced work is not feasible, companies just had an intense crash course in how to do more with less — how to operate production lines with fewer employees, how to handle customers with fewer service staff, etc. Even if the covid crisis resolves, they will not unlearn those money-saving, profit-enhancing lessons.

Our readers know that we do not believe the “robot apocalypse” model which says that automation is a dreadful danger — in many cases, we believe, it is a great boon. But the rapidity of the “covid boost” to automation could make the labor market adjustment even rockier than it would have been otherwise. Once again, that could have significant political and economic ramifications.

Investment implications: All investors, in all asset classes, should consider that even as the pandemic gradually resolves, its effects are only becoming clearer, and they may be establishing changes of trend for many assets. Technology, communications, and growth are all beneficiary themes that may experience an acceleration of their longstanding dominance. Commercial real estate, traditional retail, small companies, value, and urban density are themes which may see their fortunes enduringly impaired by the processes that the pandemic policy response has unleashed. This is not a time for investors, particularly retirees, to sit content with a portfolio whose composition has become concentrated in impaired economic sectors, or unreflective of the new risks that are being created.