The news cycle is still partly occupied with COVID-related coverage, and thus the markets will likely still respond to reports of rising cases, and advances and setbacks in vaccine trials. (We note that daily deaths are declining again in the U.S., and in some European countries have fallen to single digits.) However, political news surrounding upcoming U.S. elections, we believe, will increasingly take center stage as a driver of near-term market sentiment.

Putting Policies Side By Side

The level of partisan feeling in the United States is extremely high. Our regular readers know that we strive to be non-partisan in our research and our view of markets. Our view of the merits and demerits of political programs and platforms is practical and straightforward. We try to answer the question of what effect different political outcomes will have on investment portfolios.

Here we will take a brief look at the tax proposals of the Biden and Trump campaigns — insofar as these have been clearly articulated.

On corporate taxes: After the passage of the Tax Cuts and Jobs Act (TCJA) of 2017, the corporate tax rate stands at 21%. In keeping with his overall intention to confirm and extend the TCJA, Mr Trump has proposed a further cut to 20%. Mr Biden proposes to increase the rate to 28%, adding a 15% minimum tax of companies that report greater than $100 million in net income but owing no U.S. income tax.

One of the main changes enacted by the TCJA was to exempt earnings from active businesses of US firms’ foreign subsidiaries, even if the earnings are repatriated. To discourage the shifting of profits to low-tax jurisdictions abroad, the TCJA taxed this “global intangible low-taxed income” at a 10.5% rate — half the statutory rate for corporate income tax generally. Mr Biden would double that to the full 21% statutory corporate rate.

Both candidates have proposals that would use tax incentives to encourage reshoring of manufacturing to the United States. Mr Trump would like to extend the immediate expensing provided for in the TCJA, specifically mentioning biopharma and robotics companies who bring back U.S. manufacturing operations.

On real estate: While he has not said so explicitly, Mr Biden’s call to eliminate “unproductive and unequal breaks for real estate investors” is widely interpreted as indicating his desire to repeal the “like-kind” exchange rules (e.g., the “1031 exchange”) that permit many real-estate transactions to avoid incurring taxes on realized gains. If carried through this would have a profound impact on many real estate investors; we can be sure that it would face profound resistance from powerful lobbying groups. Mr Trump has not proposed changes to these exchange rules.

On financial institutions: Mr Biden would impose a “risk fee” on certain large, systemically important financial institutions.

On energy: Mr Biden would repeal certain tax exemptions and favorable treatments for oil, gas, and coal producers. He would also promote a raft of incentives and subsidies for alternative energy, such as making the solar ITC permanent; expanding deductions for emissions-reducing investments; increase incentives for electric vehicles; and create tax incentives for renewables and low-carbon technologies. Mr Trump favors further reductions to these green incentives and subsidies.

On individual taxes: Mr Biden would raise the top rate on ordinary individual income tax to 39.6%. Mr Trump would make permanent the current 37% top rate, and has suggested a middle-income tax cut, but has not made a formal proposal. Mr Biden would tax long-term capital gains as ordinary income for those with taxable income greater than $1 million; Mr Trump would like to reduce capital gains taxes from current levels, but has offered no formal proposal.

On Social Security: Mr Biden proposes to expand Social Security tax to apply to wages above $400,000.

On estate taxes: Mr Biden has proposed raising the top estate tax rate to 45%, and eliminating the “stepped-up” basis that permits heirs to avoid paying tax on an asset’s appreciation that occurred during the decedent’s life.

On retirement savings: Mr Biden has proposed changes to the treatment of defined-contribution retirement accounts. According to the Tax Foundation:

“Biden proposes converting the current deductibility of traditional retirement contributions into matching refundable tax credits for 401(k)s, individual retirement accounts (IRAs), and other types of traditional retirement vehicles, such as SIMPLE accounts. Biden’s proposal would eliminate deductible traditional contributions and instead provide a 26 percent refundable tax credit for each $1 contributed. The tax credit would be deposited into the taxpayer’s retirement account as a matching contribution. Existing contribution limits would remain, and Roth-style tax treatment would be unaffected… Compared to current law, the flat credit would provide a larger benefit to lower-income earners and reduce the benefit to higher-income earners.”

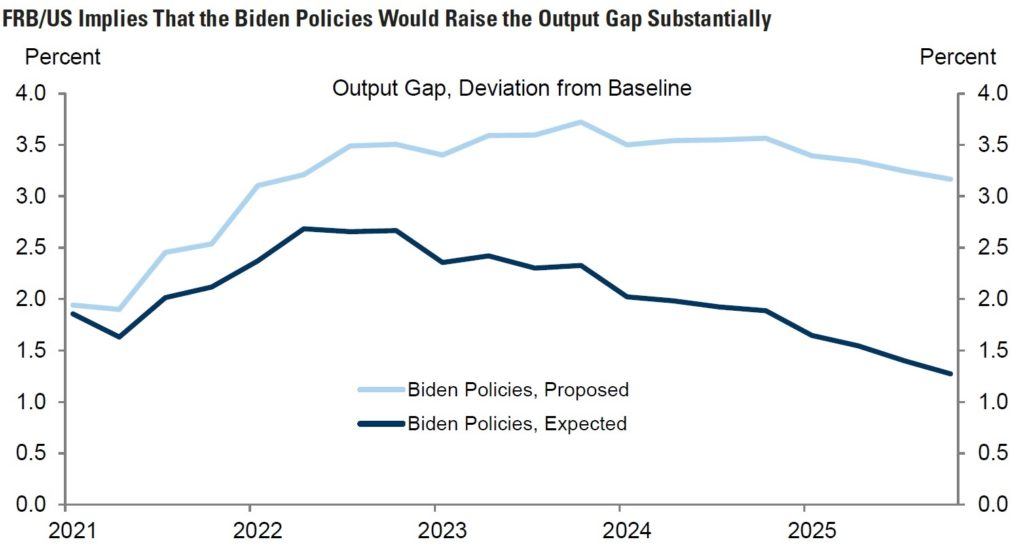

In sum, Mr Biden’s proposals would substantially increase Federal spending, partially offset by higher corporate and personal taxes. In turn, this would increase the “output gap” — the difference between potential and actual GDP. The analysis below distinguishes between the effects of Mr Biden’s full policy proposals (light blue), and a 50% success in getting them through Congress (dark blue).

Many financial-market participants believe that a higher-tax, higher-regulation regime transfers economic decision-making power from the private to the public sphere, which they believe to be less efficient in capital allocation, because it is more driven by ideology, with less “skin in the game” and responsiveness to real-world success and failure. Market participants tend to believe that higher taxes and a greater role for government in economic decision-making, other things being equal, will depress growth — which would ultimately shrink the economic pie for everyone.

Investment implications: There are significant differences between the two U.S. Presidential candidates on fiscal and tax policy. On balance, market participants believe a Biden administration — especially in the event of a Democratic sweep — would implement policies that would incrementally increase the power of the Federal government to direct the U.S. economy and choose winners and losers, and would likely cause economic growth to fall below its potential. This would eventually have negative consequences for the value of many financial assets. Thus in the leadup to an election believed likely to produce a Biden victory and a Democratic sweep, a market correction is likely. Real estate investors should be particularly attentive to the prospect of a revision of like-kind exchange rules.