Looking Back on 2017

Let’s take a step back and imagine that 2017 is almost over — and that we’re looking back from a standpoint in late December.

What will we see has happened in the U.S. market during the remainder of 2017?

First, we think we’ll be reviewing a volatile year. (The current lack of market volatility is a sign that investors should be prepared for volatility after the current rally slows down.)

In summary, as regular readers probably know, we think that from the perspective of the year’s end, our current bullish view of U.S. stocks will be justified. We’d like to delve a little deeper into an explanation of this belief.

1. With no recession imminent, we believe that market selloffs that occur in 2017 will be in a normal, moderate range.

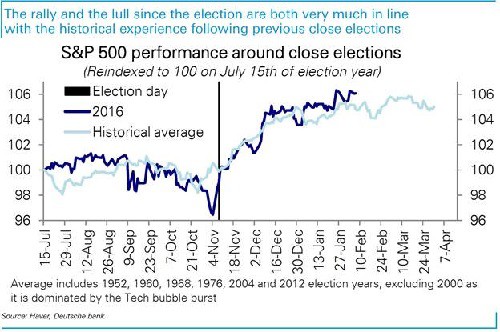

Small stock-market selloffs of 3–5% often occur every 3 months, and slightly larger sell offs of 5% or more occur, on average, every 6 months. The rally we have seen since the election is in the normal range, and Deutsche Bank has produced a very useful chart pointing out how markets react after close elections.

Source: Deutsche Bank Research

Short-term selloffs of the 3–4% or 5–7% variety often occur because of a political, military, or financial scare, but typically do not have a major driver that will cause corporate profits to fall, and thus cause stocks to fall. An example from the recent past was Brexit in June, 2016, when the U.S. market fell by about 5% and quickly reversed.

Major market corrections are far less common, and are caused by significant economic events which deeply affect corporate profits and thus stock market valuations. They occur every few years, often at the very beginning of a recession or period of economic hardship. These can be devastating, and investors or money managers should, in our view, have a policy to cut losses when the correction reaches a predetermined depth.

However…

2. In our opinion, we are not close to a situation where a major selloff will occur this year.

We believe that major selloffs are the result of economic slowdowns, which occur when shorter-term interest rates rise and exceed longer-term rates. This is known as the “inversion of the yield curve.” Higher short-term interest rates have the effect of making capital more expensive to corporate borrowers, which leads to a decrease in corporate profits — which in turn leads to a larger decrease in stock prices. This, combined with emotional reactions and fear of long-term damage to the economic system, leads to major market selloffs: for example, the bear market of 2008 and early 2009.

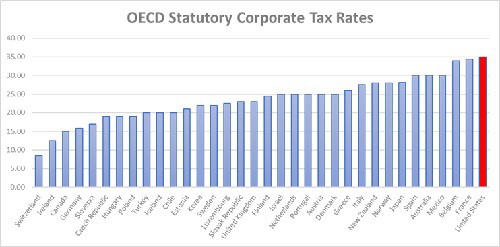

3. We see an optimistic path forward toward a cut in corporate income taxes, and eventually (probably in 2018 or 2019), a cut in individual income taxes.

Some are very concerned about a trade war. We believe that any trade frictions that occur will more than be made up for by a cut in corporate and individual income taxes. Both tax cuts will act as an accelerator to economic growth as measured by GDP, corporate profits, and stock market appreciation. U.S. statutory corporate tax rates are the highest of the developed countries:

Data Source: Mercatus Center

4. A cut in excessive bureaucracy on the national level and on the level of some state and local governments will also improve economic growth.

The pendulum of sloppy regulation on financial industries reversed itself after the economic contraction of 2008, and the result was a swing of the pendulum toward regulation that ended up stifling corporate profits and job creation in many industries. The pendulum is now swinging back toward more moderate and common-sense regulation — which will allow new businesses to form, existing businesses to grow, and the economy to add more jobs and raise the national standard of living.

5. Inflation is rearing its head around the globe, and the fear of deflation which has troubled most of the world’s economies since late 2007 is finally beginning to recede.

The new environment will support a reflation of prices on a global basis. Moderate inflation is favorable to economic growth, an increase in corporate profits, and overall economic wellbeing. The key is to keep inflation at a moderate level. The U.S. Federal Reserve wants a 2% inflation rate, and we believe that rate will be exceeded this year. In our view, inflation will reach 3% in the U.S. temporarily this year, unless the U.S. dollar appreciates excessively. This thesis was reinforced this week when U.S. CPI data for the last 12 months were released, coming in at 2.5%.

To summarize, a combination of moderate inflation with stronger capital spending by corporations will lead to a positive economic, profit and stock market environment in coming years if the current administration’s plans for tax cuts and regulatory reform are implemented. o

Attractive Areas

Given this generally bullish view of the U.S. stock market, where do we see particularly attractive opportunities? Looking back from the end-of-2017 vantage point, where will we see sectors and industries that have outperformed?

• Beneficiaries of lower taxes: all companies with effective tax rates near the 35% Federal statutory rate.

If the statutory rate is lowered towards the global average of 20%, all high-tax-paying companies will benefit. Most high-tax payers serve domestic markets and do not get to benefit from lower overseas taxes and the use of global tax havens.

Industries that fall into the high-tax group include capital goods, commercial services, diversified financials, energy, food and beverage, food retail, media, regional banks, retail, transportation, and utilities. Not all will be attractive investments — but these will be the biggest tax-cut beneficiaries.

• Beneficiaries of more commonsense regulation.

Financial institutions, credit-card issuers, stock brokers, insurance companies, banks, transportation (trucks, airlines, pipelines), natural gas providers, oil companies, and airlines.

• Beneficiaries of the move from deflationary to inflationary pressures around the world.

Commodity and industrial stocks, precious metals, base metals, energy, industrial manufacturers and distributors.

• Beneficiaries of tariffs and anti-dumping rules.

Steel, chemicals, farm products (grains, meats), base metals producers, manufacturers of transportation equipment (airplanes, trains, trucks).

Investment implications: When we look back on 2017 from the year’s end, we think that we will see a year that was marked by volatility — but also a year that will justify our current bullish outlook on U.S. stocks. Why do we think this? First, because the post-election rally and rest so far has been very much in line with the relief that markets have historically expressed after a close presidential election. We see no imminent inversion of the yield curve and no looming recession. In the absence of real economic turmoil, we think corrections will remain in the 3–7% range and will present buying opportunities. Since the post-election rally is in the normal range for rallies after closely contested elections, we think there is more upside as the new administration’s policies unfold — especially industries and companies that will benefit from lower taxes, regulatory reform, a shift in global psychology from deflation fears to inflation anticipation, and new potential tariffs and anti-dumping actions.