At this point in the post-pandemic recovery, a lot depends on who is right in the very lively “transitory vs. persistent” inflation debate. For investors, the question is particularly sharp. If you believe that Fed Chair Powell and Team Transitory are correct, you will position your portfolio quite differently than if you belong to Team Persistent.

Fed Governor Lael Brainard summed up the argument for transitory inflation in a May 11 webcast:

“To the extent that supply chain congestion and other reopening frictions are transitory, they are unlikely to generate persistently higher inflation on their own. A persistent material increase in inflation would require not just that wages or prices increase for a period after reopening, but also a broad expectation that they will continue to increase at a persistently higher pace. A limited period of pandemic-related price increases is unlikely to durably change inflation dynamics.”

Wage Inflation Now Visible

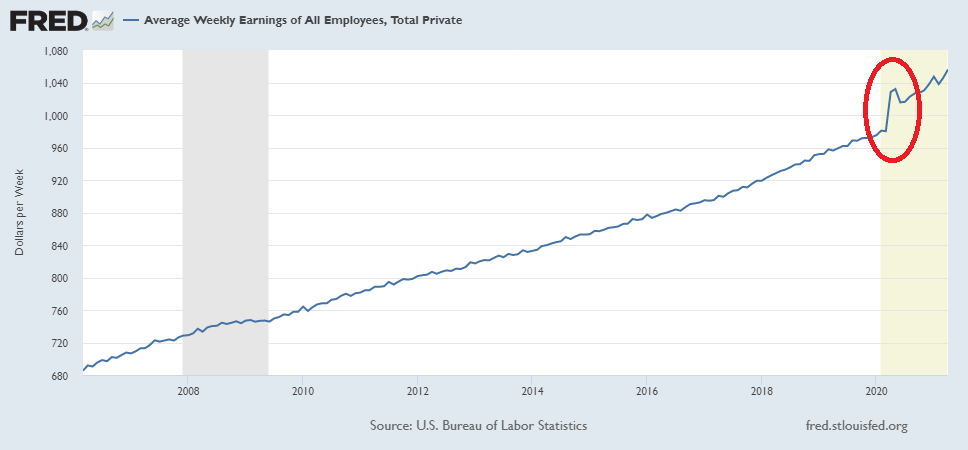

That places concern squarely on the issue of wage inflation, and on expectations for wage inflation to be persistent. So is wage inflation occurring? Here’s the raw data on average weekly earnings from the Bureau of Labor Statistics:

That chart, showing average weekly earnings of all employees in the U.S., requires some interpretation. The dramatic spike at the beginning of the pandemic lockdowns represents average wages rising, because of the mass unemployment that affected the lowest-paid workers most severely. In other words, the average rose in part because the bottom earners of the population suddenly dropped out of the calculation.

And the government stepped in to substitute helicopter money for their lost income, as shown in this chart of personal disposable income — which includes transfer payments:

But here is an interesting observation. Pandemic unemployment peaked in April 2020 at 14.8%, and at its most recent reading a year later, had fallen to 6.1%. 6.1% may seem high to recent memory but it is the same level as the country enjoyed in August, 2014. In short, as far as unemployment goes, the pandemic shock was brief.

So have average wages begun to return to their pre-pandemic trajectory? No, they have not — the line moved up, and has continued to climb. To us, this implies that there is something else going on besides statistical artifacts, and that is related to the wild spike in disposable income driven by transfer payments. March 2021 real personal disposable income was up 29.3% year on year. Virtually all of that increase was comprised of government transfer payments, which comprised about 30% of income in March.

Government Is Incentivizing Continued Unemployment

This, in turn, is certainly related to the laments of the businesses, which we have heard both statistically and anecdotally from direct contacts, that they can’t fill all the positions they need to fill. In the most recent edition of Small Business Economic Trends, published by the National Federation of Independent Business, indicates that 42% of respondents have positions they can’t fill, a five-year high. Large corporates, from Chipotle and McDonald’s to Bank of America, are raising starting wages and salaries in an effort to fill open positions.

Arizona, Montana, and Connecticut will be offering “return to work bonuses,” and they are likely perceiving the real root of the problem. Private enterprise is competing for workers with the government’s stimulus and unemployment programs.

Can Government Withdraw Pandemic Stimulus?

If inflation remains persistent, interest rates will rise, with profound effects on investment portfolios — particularly those heavy in bonds and heavy in high-multiple stocks. If wage inflation is the key to that question, the key to wage inflation is simply this: how quickly and how completely will the pandemic transfer payments be ratcheted back?

That, ultimately, is a political question. Unfortunately, we believe that now that the “Helicopter Money Rubicon” has been crossed, it will be politically very difficult to go back, even for those who want to — and we do not see much appetite to make the attempt. Expectations are high for continued elevated levels of fiscal stimulus (whether direct transfer payments or other forms of government largesse). Political fears are equally high that whoever curtails them too sharply will be punished by the electorate in the crucial 2022 midterm elections. Since it will become increasingly difficult to justify further direct stimulus to individuals, it will likely take the form, for now, of big Federal spending projects.

Investment implications: Rising wages, hiring bottlenecks, and ongoing large transfer payments are an indication that inflation is not likely to be as transitory as Fed optimists believe, in our view. Therefore, as we note below, we believe that investors should continue to position their portfolios for more persistent inflation, by reducing their holdings of high-price-to-earnings stocks, and adding on dips to commodities, including precious and industrial metals (particularly gold, silver, copper, lithium, zinc, nickel, and rare earths). Commodity-centric markets, particularly those in the developed world such as Canada, may benefit both from the global inflation trend and from the weakness of the U.S. dollar.