While listening to the recent round of quarterly conference calls, we noted that most managements were still discussing supply-chain issues — and saying that these were problems that have not yet been resolved.

Trans-Pacific spot shipping rates remain elevated. The Port of Los Angeles, which receives a third of all U.S. imports, has seen its backlog continue to increase, driven by port closures in Asia, labor and container shortages, warehousing and trucking issues, and Chicago rail disruptions. The port’s manager does not believe that the situation will substantially improve until November, though even that is contingent on the pandemic situation not deteriorating further.

Underlying the various factors mentioned by the L.A. Port manager, as well as many company managements, we see a common thread — labor. This may be a key factor in much of the supply chain disruption being experienced, particularly in the U.S., where perverse incentives are still keeping many workers from seeking available jobs. That is a situation that will begin to normalize at the beginning of September when (if?) Federal pandemic supplemental unemployment benefits are terminated.

It is our guess that this is a significant contributor to many supply chain issues. In September, we’ll see if there is any appetite among lawmakers to ratchet back some of the experiment in Modern Monetary Theory that has been ongoing since the beginning of the pandemic. If pandemic benefits remain in place, we think supply chain issues will be slower to improve.

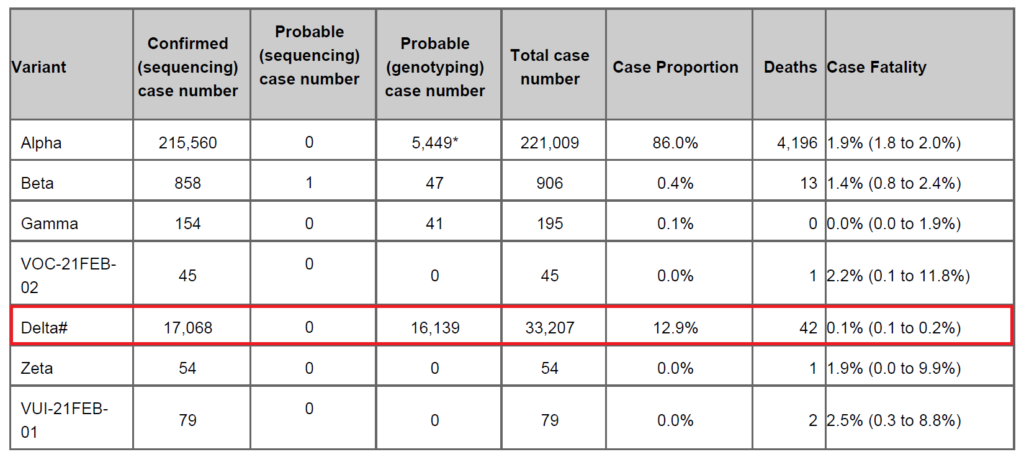

As far as the Delta variant goes, we noted the following chart in the U.K. government’s June publication monitoring covid variant strains:

Source: Public Health England

The case fatality rate for the Delta variant is between 10% and 20% that of Alpha, the original strain. This is the pattern that evolutionary virologists expect; newer strains of a respiratory virus typically show enhanced transmissibility and reduced lethality (i.e., evolutionary “success” from the virus’ point of view). Therefore despite media alarm, we anticipate that the Delta strain will peak and begin to decline. Some analysts believe that peak has already occurred, with weekly cases still growing but decelerating from a late-July peak.

A recent piece in the Financial Times reinforced our opinion of the likely reasons for quick contact between Afghanistan’s new rulers and the Chinese. Pentagon analysts believe that Afghanistan has lithium reserves tied with Bolivia to be the world’s largest, in addition to substantial reserves of rare earths and other strategic minerals.

Whether the Chinese can make any headway in creating an infrastructure to allow for the extraction of this mineral wealth is of course another question. (Those assuming that China’s rulers and the Afghan population will easily find common ground should consider that China cannot even coexist with its own Muslim population, the Uyghurs of Xinjiang — a fact of which the Taliban are well aware.)

We continue to favor tech and tech-enabled themes, as well as some tech-related commodities such as copper and lithium. As we have told you in many recent letters, we believe that the tech themes accelerated by the pandemic — particularly business digitization, financial technology and financial services, remote and hybrid work infrastructure, cybersecurity, innovative biopharma, medical technology and services, and online training systems — will be enduring. We would be buyers of these themes on weakness.

Thanks for listening; we welcome your calls and questions.