In many respects, a relative goldilocks period seems to be ending. Growth, revenue, and profit recoveries have lapped pandemic lows. Further direct consumer stimulus is not forthcoming. Further broad fiscal stimulus is running up against more significant Congressional resistance, and scorched-earth warfare over the debt ceiling may be approaching.

The 2022 midterm elections are beginning to come into view. The sense is palpable among some more activist members of the Democratic Party that now is the time to push through bold agendas, because if those midterms go poorly, they may not get another chance for a long while. Others feel that pushing too hard would alienate the great center which still represents most Americans — even if those on the coasts and in the largest cities can’t believe that any Americans exist outside the hyper-partisan bubble in which they live and breathe.

The JOLTs job opening report showed an extraordinary 2.2 million openings more than unemployed workers. This is a postcard of the kind of pandemic policy disruption that is ongoing, across the labor market and a host of global supply chains. As the Fed’s Beige Book succinctly commented, “Many businesses reported having trouble sourcing key inputs.” Not simply inflation — shortages.

Add this confounding mixture to weak seasonals, apparently rising geopolitical risks between the U.S. and China, and the ongoing aftershocks of the U.S. withdrawal from Afghanistan, and there is plenty of opportunity for weakness into year-end.

Still, as we have emphasized week after week, these worries are piling up against a backdrop that remains fundamentally positive: of ongoing, if uneven, economic recovery, and relentlessly plentiful liquidity.

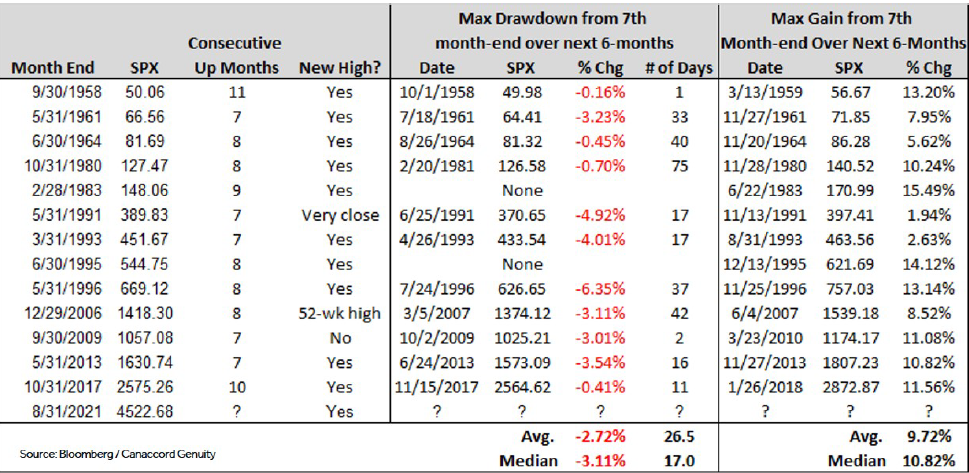

Canaccord’s Tony Dwyer helpfully broke down historical instances of markets with a streak of seven positive months, as we have just enjoyed:

Source: Canaccord Genuity

The takeaway? In the six months that followed such a streak, the worst drawdown was 6.35%, and average gain was 9.7%. It’s only history, and as we know, “past performance is not a guarantee of future results.” However it does suggest to us that overly pessimistic sentiments are likely setting investors up to miss an opportunity.

If volatility does arise, we believe that volatility will be an opportunity to buy the enduring themes in software, hardware, healthcare, medical technology, and fintech that we have favored for many months.

Thanks for listening; we welcome your calls and questions.