Water, and the state of U.S. drinking and wastewater systems, entered into the mind of U.S. investors during the Flint water crisis back in 2014. Since then, an acceleration has occurred in domestic water infrastructure spending, coinciding with rapid technological advancements — smart metering, the internet of things, big data analytics to inform system construction and operation, etc. Large swaths of the U.S. water system are reaching or have passed the end of their useful life, presenting both the need for investment and the opportunity to do it in a way that harnesses new technologies.

Source: Goldman Sachs Equity Research

Until the pandemic arrived, investors were faced with the question of the sustainability of this momentum, and whether it would translate into an investable opportunity, given the highly fractured nature of the water industry in the United States. The U.S. has more than 51,000 community water systems (CWS); 8% of systems serve 82% of the population. Sufficient investment is difficult for a CWS absent acquisition or a bolus of infrastructure spending, and would lead to indigestible rate increases.

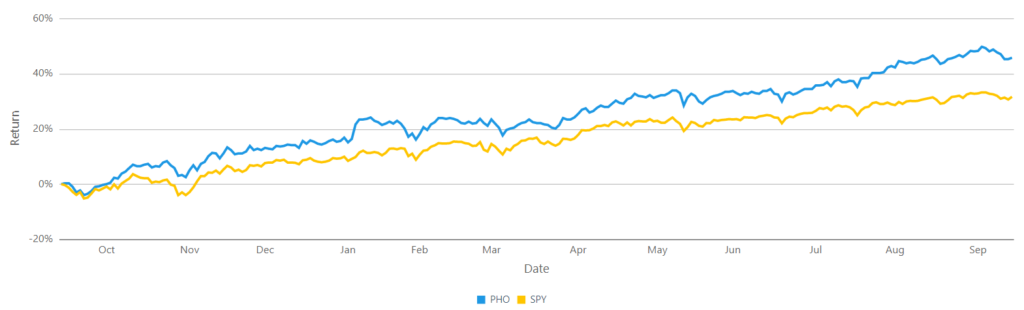

That bolus of spending is beginning to arrive, courtesy of the Biden administration’s massive infrastructure push, the American Jobs Plan; the market has been anticipating this spending for some time. Over the past 12 months, the Invesco Water Resources ETF [PHO] has handily outperformed the S&P 500, 45.7% to 31.6%.

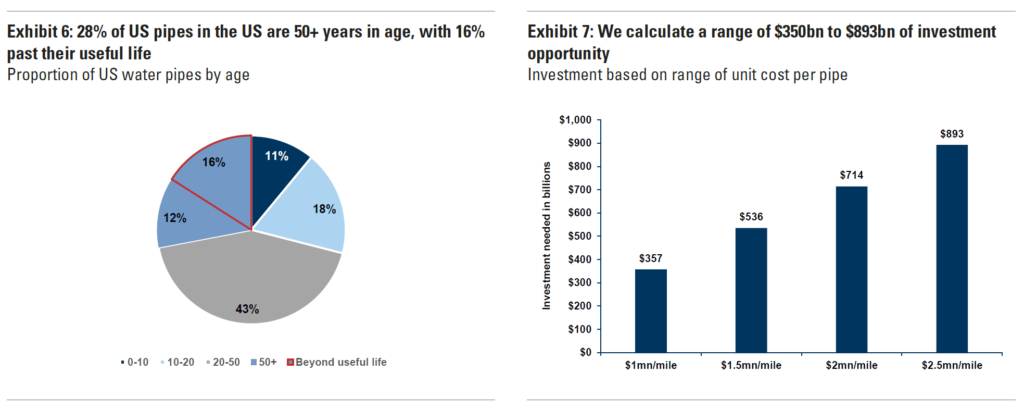

The agony of congressional infighting is ongoing, but the $110 billion initially earmarked for water spending seems to be surviving political battles unscathed. Separately, a proposal has been made in the Senate for an additional $35 billion Drinking Water and Wastewater Infrastructure Act. However, the truth is that the need — conservatively, $250 billion; perhaps as much as $800 billion — dwarfs the allocations described above. Given what looks like a bipartisan sea-change in attitudes towards deficit spending, it is likely that more funding is coming.

Increasing regulation to encourage energy efficiency and sustainability is also likely on the agenda. Manufacturers of hardware such as pumps, valves, controllers, and meters are likely beneficiaries. And of course, now, no politician wants to be in a jurisdiction where anything like the Flint debacle occurs on their watch. This is one ESG area where die-hard environmentalists, and those who are more skeptical of the ESG agenda, can agree that spending is critical.

Even aside from the swelling tide of government infrastructure spending, some of the pandemic trends that are likely to be enduring will boost the fortunes of many companies in the water industry. Residential construction spending has been experiencing double-digit growth since 2020; this likely reflects pandemic tailwinds as work-from-home has shifted spending priorities towards homes. Analysts expect this trend to continue for the rest of 2021. Housing starts will also contribute.

Rising materials costs are potential headwinds. However, manufacturers in this space are in a good position to defend margins and pass rising input costs on to their customers, whose demand is largely price inelastic — either because they are publicly funded, or because their products are deemed essential in construction and maintenance.

Investment implications: Water has performed well in the lead-up to the passage of some form of the administration’s infrastructure bill. Many elements of the administration’s aspirational wish-list will suffer the axe before the bill is passed, but water infrastructure spending is not likely to be among them. The runway for water spending is long, the need is high, and the potential benefits from digitization are extensive. There are several large ETFs that investors can use to gain broad exposure to the industry; our recommendation would be to lean towards companies whose operations and revenue primarily come from the United States.