Another week brings another set of inflation-related data to report on. In the past few days, we have seen consumer (CPI) and producer (PPI) inflation data from the U.S., Europe, and China. (When our October data are complete next week, we’ll give you an update on our in-house real-world inflation measure, the Guild Basic Needs Index. Here’s a teaser — it’s north of 30% year-on-year.)

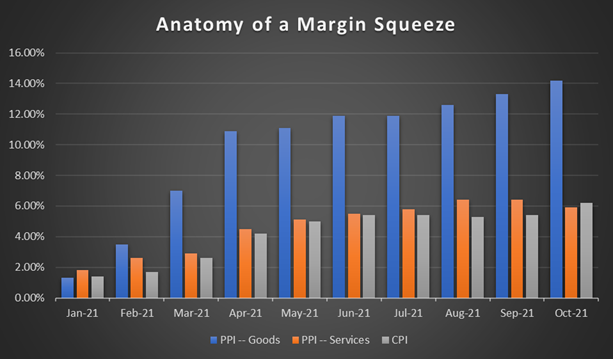

The spread between U.S. CPI and PPI is a rough indicator of margin pressures faced by businesses economy-wide. Of course, different sectors and industries will suffer this squeeze to very different degrees — offering investors a useful starting point for evaluating areas of interest in coming months. In particular, tech-focused services industries are more attractive to us than producers of finished goods.

Guild Investment Management

Data Source: Bureau of Labor Statistics

This impression becomes sharper when we remember that the performance of the S&P 500 over the period that followed the Great Financial Crisis was driven significantly by expanding profit margins. Thus far, businesses index-wide have been able to hold the line; the graph below shows trailing 12-month profit margins for the S&P 500 continuing to rise to new all-time highs. The question is what this graph will begin to look like as we lap “V Day” (the announcement of Pfizer’s vaccine on November 9, 2020) and roll forward into 2021’s very different environment. This is one instance where the potential causes of “mean reversion” are fairly clear.

S&P 500 Profit Margins At All-Time Highs

Source: Bloomberg LLP

Wages and Productivity

Productivity presents a compounding problem. At the November 3 press conference following the FOMC meeting, Fed Chair Powell commented:

You know, the concern is a somewhat unusual case where if wages were to be rising persistently and materially above inflation and productivity gains, that could put upward pressure on or downward pressure on margins and cause companies to their employers really to raise prices as a result, and you can see yourself, find yourself in what we used to call a wage price spiral. We don’t have evidence of that yet. Productivity has been very high.

The comment was somewhat confused, but it shouldn’t be ignored.

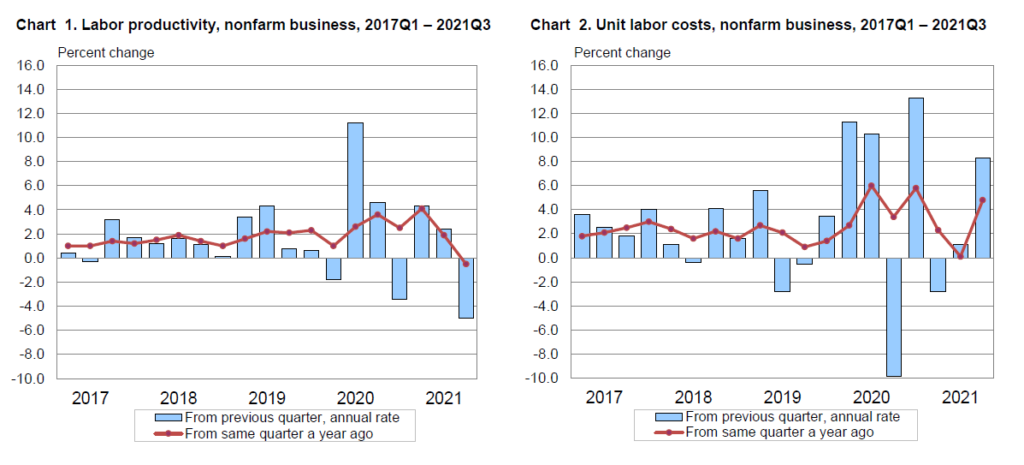

Unfortunately, the next day, data came out from the BLS showing productivity taking a sharp dip in Q3 2021, the sharpest since the 1980s, even as wages spike.

Source: Bureau of Labor Statistics

Here, then, is a further data point suggesting margins will need to revert from all-time highs: wages are rising more than productivity — and this spells trouble particularly for labor-intensive sectors and industries. Fed Chair Powell noted that such wage inflation would have to be persistent to be a problem — but as we noted last week, there are significant reasons to believe that there are indeed persistent economic trends underlying current wage growth. Perhaps Mr Powell will be happy if he is replaced next year by Lael Brainard.

“The Great Retirement”

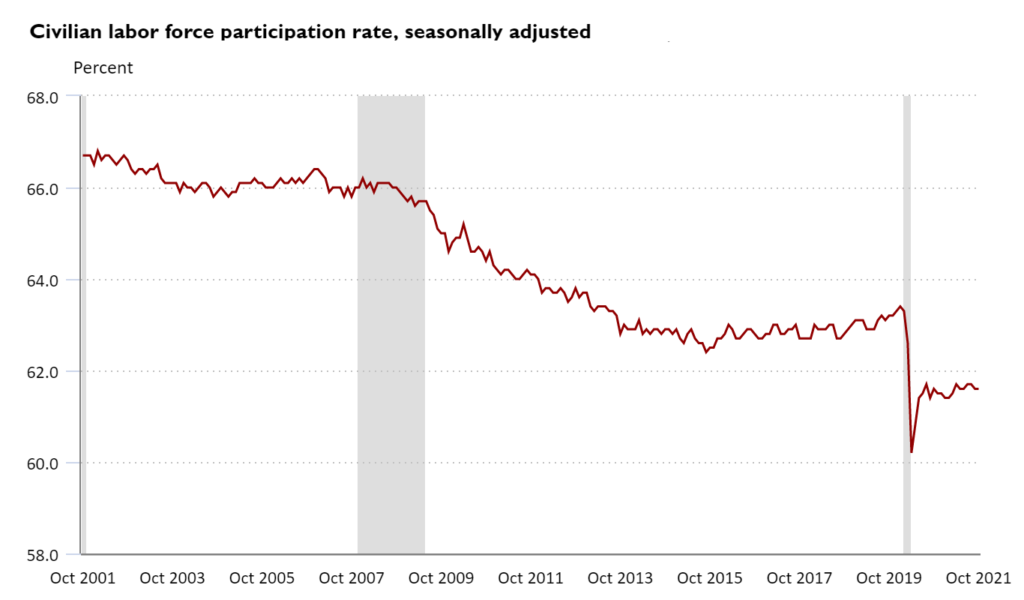

Last week, we noted trucking as a critical occupation where retirements may have been pulled forward by the pandemic. Of course, it is not the only one. The labor-force participation rate has recovered somewhat from the pandemic lows, but since then has “stalled,” reinforcing the possibility that the decline is persistent.

Source: Bureau of Labor Statistics

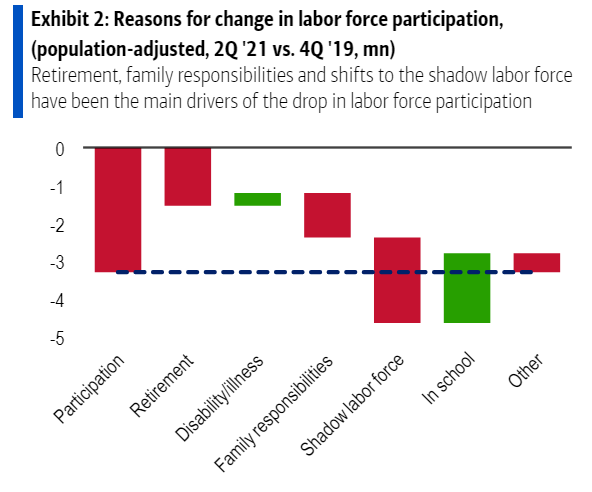

An attempt to figure out where the “missing workers” have gone shows that indeed, sooner-than-expected retirement is a major culprit, accounting for about half of it. Add in “family responsibilities” — care for children and for elderly relatives, which may reflect new pandemic-driven lifestyle choices — and you have most of the decline.

Source: BofA Global Research

Investment implications: Producer price and consumer price inflation data taken together suggest that record high corporate profit margins are likely to revert — challenging particularly goods manufacturing industries and companies with high material and labor cost inputs. Thus we broadly prefer services businesses, and some providers of raw materials, to goods producers. A recent dip in productivity suggests also that businesses with strong productivity growth will be better positioned to perform during prolonged inflationary “bad weather.” Taken together, this reinforces the case for the renewed leadership of tech and growth, with the addition of critical materials suppliers, including suppliers of lithium, rare earths, battery minerals, and other tech-essential inputs. We like businesses whose labor exposure is weighted towards the higher end of the wage structure, which again argues for tech broadly, financial technology, medical technology, process automation, and software. It also argues for legacy operators or new entrants in traditionally labor-intensive fields, such as logistics, who are able to leverage technology effectively to boost productivity growth.