How To Understand Current Volatility, and What To Expect

Markets are beginning to digest the arrival of higher rates and the start of the Fed’s balance-sheet runoff. Even more than usual, there is a host of cross-currents influencing markets as the aftershocks of the pandemic continue to reverberate through the financial system, the economy, and the body politic. Still, the belated shift in Fed messaging and policy is unquestionably the central factor currently at work — and barring geopolitical or global health black swans, will likely remain the central factor for the rest of 2022. What’s happening right now is a repricing of assets on the basis of Fed policy.

While we’re not ready to call an “everything bubble,” as some commentators have been doing for some time, there are certainly many areas of the stock and bond markets that went far into bubble territory during the pandemic. Last year’s boom in SPACs and IPOs has not aged well. (SPACs are companies that come public through reverse mergers, avoiding the more lengthy and intensive scrutiny given to traditional initial public offerings.) Many of those offerings were of interesting companies in thematically compelling areas — a lot of tech and software, closely related to the emerging suite of “Fourth Industrial Revolution” technologies such as AI, machine learning, big data, decarbonization and sustainable materials, cybersecurity, bioinformatics, telepresencing, business digitization, fintech, and so on. Our belief that these are critical investment areas to monitor for the next decade is undiminished. But as seasoned investors have learned — and a new crop of “diamond hand” Redditors is now learning — compelling themes at the wrong price are poor investments.

It’s the Normalization, Stupid

The euphoria fueled by the pandemic fiscal and monetary supernova is experiencing its inevitable comedown. Sane and normative valuation metrics and methodologies are reasserting themselves as the punchbowl drains and sobriety returns somewhat. This is a completely normal and expected process that shouldn’t be the occasion for anxiety. The process has further to run. Traders can try to trade the volatility, but in our view, valuations of the highly overvalued sectors, industries, and themes have not yet corrected enough overall to warrant serious commitment from long-term investors. We believe there will be better opportunities ahead. In the meantime, long-term investors content with their entry price can simply hold high conviction investments through the volatility.

Since the beginning of earnings season, a combination of earnings beats and price declines has seen the S&P 500’s trailing price-to-earnings ratio decline from about 26 to under 23. The very long-term normative P/E ratio is 15; in the past decade — fueled by post-financial crisis monetary policy and the relentless rise of price-agnostic passive inflows — it has been 20, which seems an appropriate level for current conditions. To us, that suggests that broadly there’s further price downside to go to reach normalization — with the additional caveat that markets typically do not stop neatly at their destination, but often overshoot it slightly. Index-level earnings growth this year will be a significant deceleration from 2021’s blistering pace. So we can expect further volatility as the monetary policy landscape evolves, blunted somewhat by rising earnings.

The Paths Forward

We see three basic potential directions for the U.S. stock market in the remainder of 2022.

The first, and most likely in our view (call it a 50% likelihood): a middle “muddle through” path, with neither a recession sparked by a Fed policy mistake, nor the arrival of embedded stagflation due to a Fed policy mistake on the opposite side. In this scenario, the Fed neither tightens faster than the economy can take, nor blinks and backs off any tightening when market volatility ensues. It is unlikely to be an inspiring, blow-the-roof off situation in any event — but it would be as “Goldilocks” as we could hope for under the current conditions of inevitable normalization. In this scenario, we would expect a volatile first half to the year, with some recovery and stabilization in the second half (bearing in mind, of course, that midterm elections will be happening in the fall).

The second (call it a 25% likelihood): a recession, resulting from excessive Fed tightening, perhaps a panic response to rising and persistent inflation and the realization that they have waited far too long to act. (Historically this is not an uncommon outcome; despite all the pretensions of academic certainty, no technocrat could ever be competent at managing a monster as huge, complex, and organic as the U.S. economy.) The recession could be mild or serious, and of varying length; the outcome would depend on the willingness of Fed officials to give, and U.S. policymakers and electorate to take, the necessary medicine. More medicine = shorter recession and better outcome.

The third (also perhaps a 25% likelihood): the arrival of stagflation — embedded high inflation coupled with muted economic growth. In this scenario, perhaps, the Fed does something about inflation, but not enough. A wage-price spiral gains traction. Well-run companies with pricing power situated in certain industries are able to convert inflation into a multiple of earnings growth — perhaps seeing a 15% increase in earnings from a persistent 7% inflation rate.

Each of these scenarios argues for a different approach to the market.

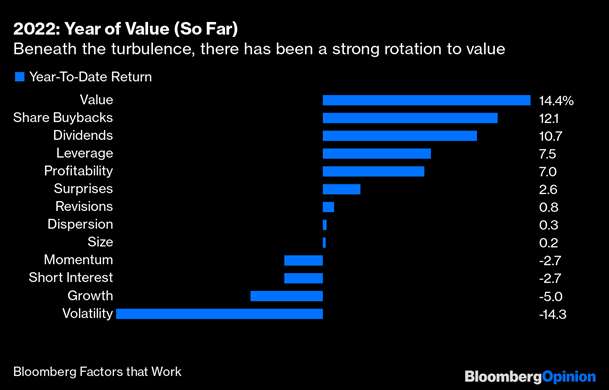

The middle road suggests caution, tactical trading, and a rotation of interest towards the beneficiaries that have shown relative outperformance as the current correction has unfolded. Remember, although it’s been more dramatic recently, it’s been underway and gaining momentum for months. The extremely overvalued stocks, such as the ARK funds, began declining a year ago. They fell first, and the carnage gradually widened until even NASDAQ leadership was declining. In relative terms, other factors have outperformed:

Source: Bloomberg, LLP

While this “muddle through” scenario is not the most inflationary of the three paths we’re describing, it still involves persistent inflation substantially above recent trends. Consequently, this is a scenario that favors inflation beneficiaries, including legacy hydrocarbon energy producers, precious metals and miners, industrial materials, and high-tech materials. Those manufacturers who have secured the availability of cheap raw materials will have operating leverage. Although digital currencies are highly speculative and currently trade like risk assets, they are still worth attention in this scenario as (if?) they develop towards being a more defensive and uncorrelated “digital gold.”

The recession road suggests our usual recession policy: a defensive posture in terms of stock allocations and higher cash balances for the more tactically oriented; and for more long-term oriented investors, patiently holding high-conviction long-term positions, and patiently waiting to deploy cash when there are signs of light at the end of the tunnel that are not an oncoming train. (However, see our comments below on cash.)

The stagflation road suggests a dumbbell allocation to “growth at a reasonable price” on one side, and a more significant allocation to commodities and some commodity producers on the other side. We would look for disruptors for the growth half of the equation, but decidedly not the speculative, overvalued, profitless wonders of the SPAC and IPO Class of 2021. Our favorites here would be large-cap tech growth with fortress-strength balance sheets, robust cash flow, and pricing power for their products.

There Will Still Be Bull Markets To Find

The bursting of a speculative bubble should not blind us to the reality that many companies whose stocks were caught up that bubble are excellent businesses and strong innovators. The bubble was driven by excessive liquidity and the irrational exuberance that accompanies it. The bursting of the bubble is to be welcomed, not feared, by the discerning investor, because it will afford an opportunity to buy exceptional companies at more reasonable valuations — and thus with a greater prospect for long-term gains. Price matters, even in an investment environment distorted by price-insensitive inflows to passive investment strategies. Those passive inflows will continue as workers earn and contribute to their IRAs and 401Ks, and indeed, they will increase nominally as wages increase nominally.

Even in our most-likely “muddling through” scenario, we believe that bull markets will pop up throughout the year in particular areas, and we will be looking for them. The change of central bank tailwinds to central bank headwinds has been anticipated and feared by markets… but of course in this case as in others, the fear is likely more fearful than the thing feared, and will drive overreactions that investors will be able to use to their advantage.

The Changing Face of Cash

On the topic of cash, we note that in an environment that is newly inflationary, with the magnitude and trajectory of that inflation unknown but worrisome, and slow-creep monetary debasement gaining steam, cash itself is a kind of “risk asset.” Given this reality, our tactical approach in the face of volatility and inflation includes recognizing that cash allocations have longer-term negative returns. Cash helps smooth out a volatile environment, but over the longer term “being out of the market” will often be as uncomfortable as being in.

An Additional Layer: Politics and Geopolitics

All of the above is predicated on a steady-state political and geopolitical environment, which is never the case, particularly not in 2022. In domestic politics, the U.S. will see congressional mid-term elections in November, and these elections will be consequential — potentially handing control of both houses of Congress to the current opposition party. From a market perspective, that would entail both positives and negatives; however, in any event, it will occasion uncertainty and likely volatility — as well as market efforts to front-run potential beneficiaries of a change of power.

Geopolitically, there is a current flashpoint in Ukraine, and heightening tensions between Russia and the west; although a conflict there would be particularly significant for Europe, we do not believe that the west has the stomach to make an existential commitment to Ukraine.

China remains a more fundamentally concerning issue; it is a rising global superpower with global ambitions and a nearly century-old bone to pick about Taiwan. The U.S. has suffered a number of recent debacles that have emboldened anti-U.S. regimes around the world, some of whom may decide that to undertake action now is preferable to later, when a more tough-minded foreign policy might again be in place in the U.S. We will be watching for any indications of Chinese intentions towards Taiwan after the conclusion of the Olympics.

It is shaping up to be a challenging and potentially rewarding year for investors. As one of our old stock-market friends (a very successful investor) likes to say at moments of particular market volatility, with tongue firmly in cheek: “Having fun yet?”

Thanks for listening; we welcome your calls and questions.